The Federal Reserve held interest rates steady at 4.25%–4.5% for a fourth consecutive meeting, maintaining a cautious stance amid persistent economic uncertainty. Policymaker projections revealed a growing divide, with half expecting no rate cuts this year and the other half still pencilling in two. Chair Jerome Powell reiterated that while the U.S. economy remains resilient, it continues to face headwinds from trade frictions and heightened geopolitical risk. He acknowledged that tariffs may temporarily lift inflation but emphasised that the Fed remains on a gradual easing path – not a sharp pivot.

This week’s U.S. data painted a mixed picture. Retail sales fell 0.9% in May, and housing starts dropped to a five-year low, underscoring ongoing pressure in the residential property sector. Mortgage applications and building permits also softened. However, consumer sentiment rebounded, with the University of Michigan index rising to 60.5 in June, reflecting improved household confidence on the back of disinflation and stable employment conditions. Political and fiscal risks, however, are adding fresh uncertainty. Trump’s proposed tax-and-spending package, along with escalating tariff threats, could add nearly $3 trillion to the national debt. At the same time, rising tensions in the Middle East have supported safe-haven demand.

The Bank of England also held its policy rate at 4.25%, with a dovish tilt as three of nine committee members voted in favour of a cut. Governor Andrew Bailey noted that interest rates remain on a “gradual downward path,” supported by softening data. UK CPI rose just 0.2% in May, while services inflation eased to 4.7%, in line with expectations. Having already cut twice this year, markets are now pricing in two further BoE rate reductions before the end of 2025.

Across Europe, monetary easing gained traction. The Swiss National Bank cut rates to 0%, and Norway delivered its first cut in five years. Inflation across the eurozone remained subdued – Germany’s CPI rose just 0.1%—while industrial production fell 2.4%. Despite weaker economic indicators, sentiment improved, with Germany’s ZEW economic expectations index increasing to 47.5. European Central Bank officials reiterated a flexible, data-dependent approach, keeping the door open for further easing should inflation remain muted.

In Japan, the Bank of Japan kept rates at 0.5% and signalled a slower pace of bond purchase tapering to avoid market disruption. Inflation accelerated, with core CPI rising 3.7% in May – the highest in two years – raising speculation of another rate hike later this year. Trade data disappointed, with exports down 1.7%. Prospects for tariff relief dimmed after talks with the U.S. failed to yield progress, and Japan now faces higher U.S. import levies from July.

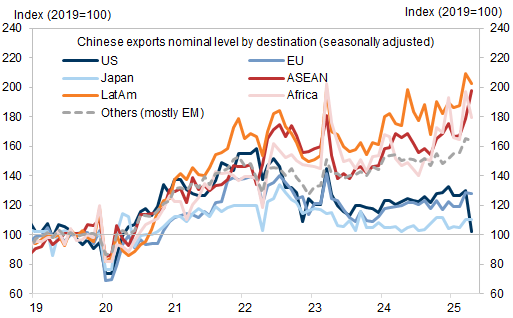

China’s May data reflected a two-speed economy. Retail sales surged 6.4%, supported by consumer promotions and government incentives, while industrial production and fixed-asset investment came in below expectations. The property sector remains a key drag, with new home prices posting their sharpest monthly decline in seven months and real estate investment down 12% year-on-year. Economists warn that further price declines could push many homeowners into negative equity, threatening broader financial stability.

Policymakers are expected to announce additional stimulus measures at the upcoming Lujiazui Forum, although several local governments have already exhausted their subsidy allocations. Geopolitical risks have also intensified, with Taiwan blacklisting key Chinese tech firms and the U.S. increasing diplomatic engagement with Taipei.

Tensions in the Middle East escalated further, with Israel and Iran exchanging missile strikes and the humanitarian situation in Gaza deteriorating. Rising civilian casualties prompted sharp criticism of the U.S.-backed aid distribution model. Oil prices surged on the back of the conflict, fuelling stagflation concerns. According to the Fed’s own modelling, a $10 rise in oil could increase U.S. inflation by 0.4% and reduce GDP by a similar margin – highlighting the policy dilemma central banks face if inflation accelerates while growth slows.

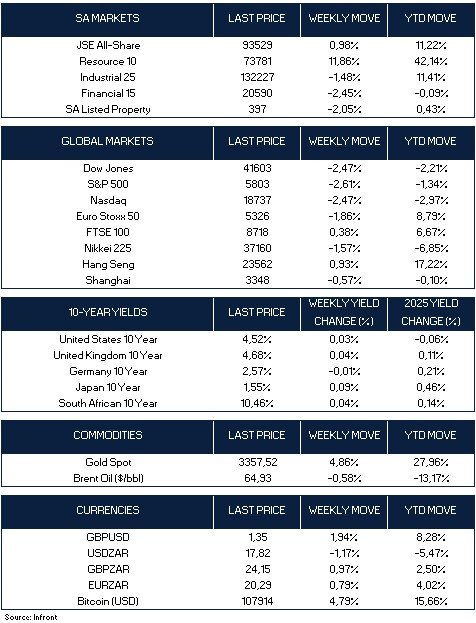

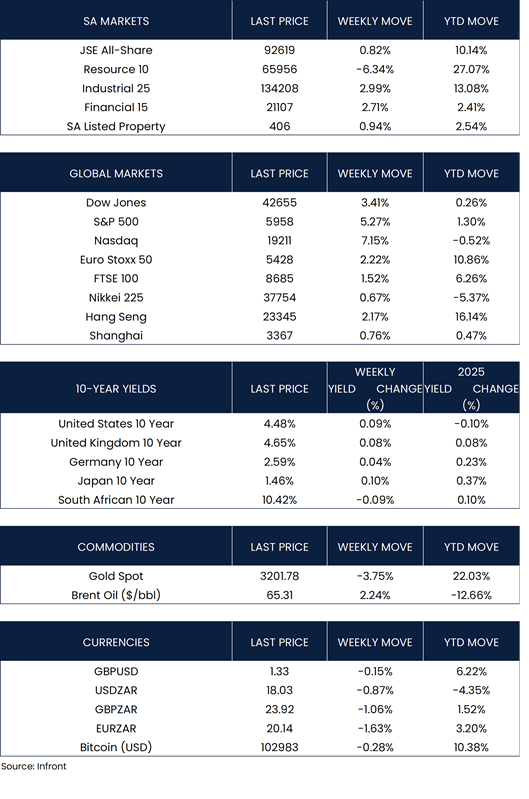

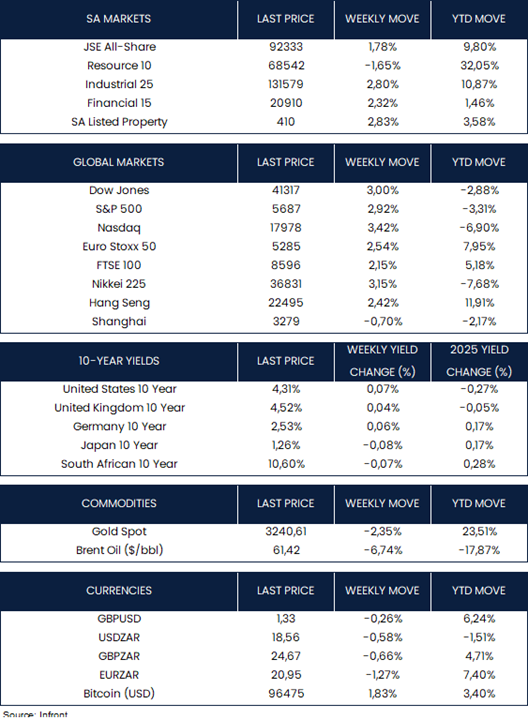

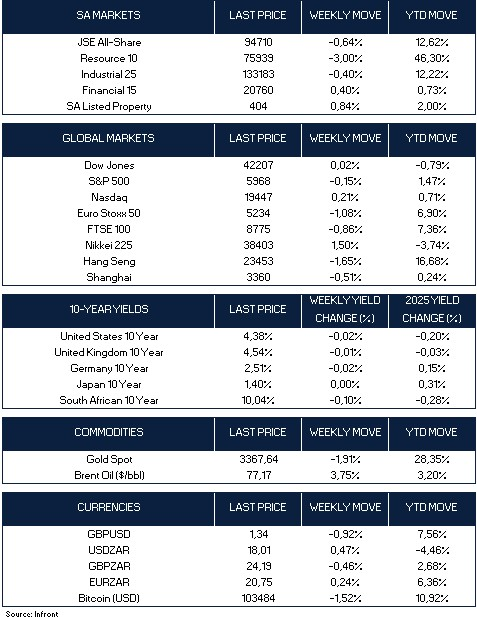

In response to the week’s developments, global equity markets were mixed. In the U.S., the Dow edged up 0.02%, the Nasdaq gained 0.21%, and the S&P 500 slipped 0.15%. European markets saw broader declines, with the Euro Stoxx 50 down 1.08% and the FTSE 100 losing 0.86%. Japan’s Nikkei advanced, while Chinese indices underperformed. Gold retreated 1.91% to $3,367.64, while Brent crude surged 3.75% to $77.17, reflecting the elevated geopolitical risk premium in commodities.

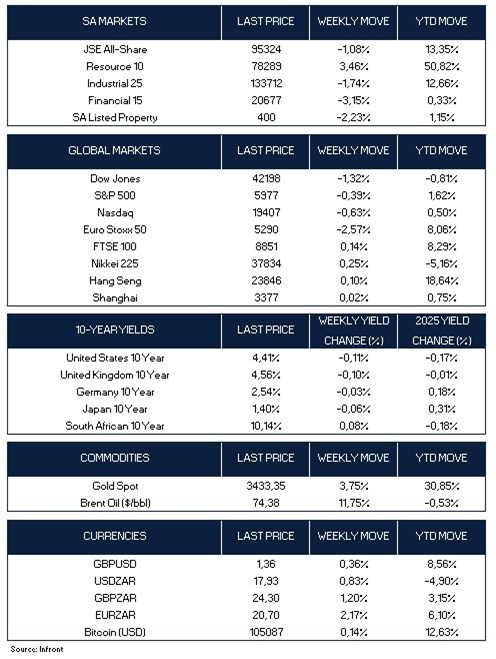

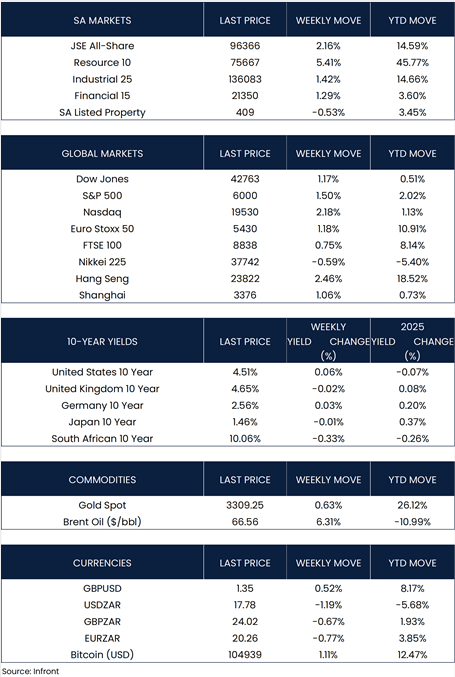

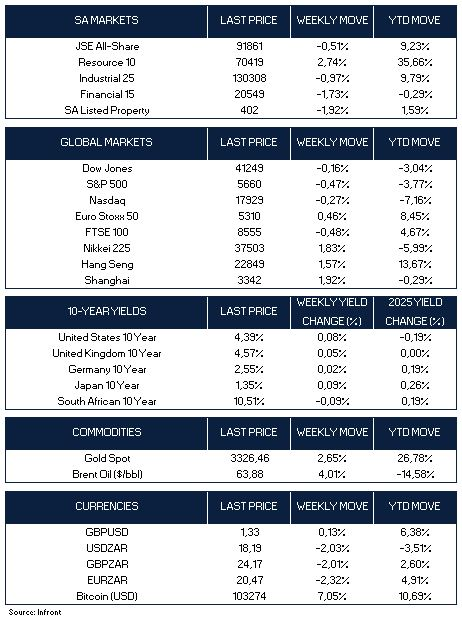

Market Moves of the Week:

In South Africa, inflation remained well contained, with headline CPI unchanged at 2.8% in May and core inflation steady at 3.0%. Despite the subdued inflation backdrop, the South African Reserve Bank has maintained a relatively cautious stance, drawing criticism from some quarters for being too restrictive. That said, the SARB has cut interest rates at three of its last five meetings, reducing the repo rate by 25 basis points at each of the first three meetings of 2025, as it continues to advocate for a lower long-term inflation target.

Retail sales data provided a more upbeat signal. April sales rose 5.1% year-on-year, a notable rebound from March’s revised 1.2% gain. On a seasonally adjusted basis, sales increased 0.9% month-on-month, pointing to some resilience in household consumption. On the infrastructure front, South Africa is courting private capital to support a R450 billion transmission grid expansion. The World Bank is considering a $500 million credit guarantee facility to help unlock financing for the project, which aims to add 14,500 km of transmission lines over the next decade. The SARB’s recent climate stress test also found domestic banks broadly resilient to environmental risks, despite persistent data gaps.

South African equities ended the week weaker, with the JSE All Share Index falling 0.64%. Resource stocks led the declines, down 3.00%, while industrials slipped 0.40%. Financials and listed property provided some offset, gaining 0.40% and 0.84%, respectively. The rand lost ground against the U.S. dollar, closing at R18.01, as global risk sentiment turned more cautious.

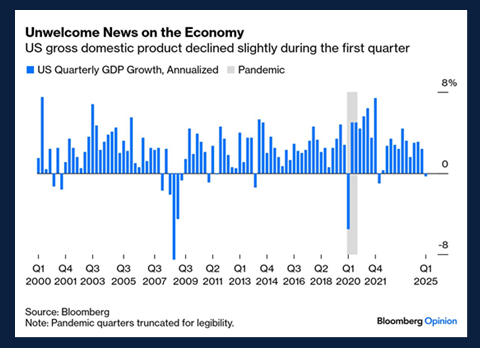

Chart of the Week:

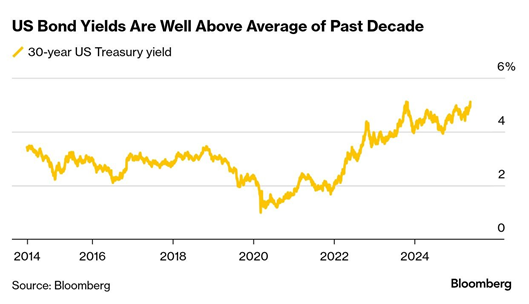

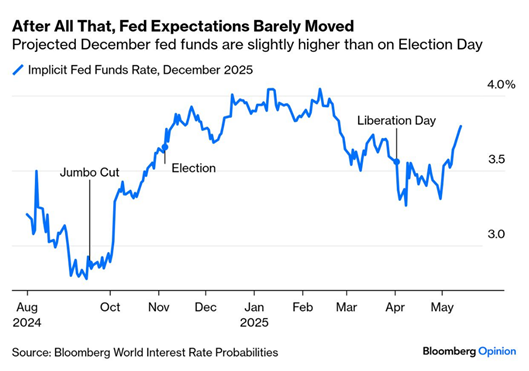

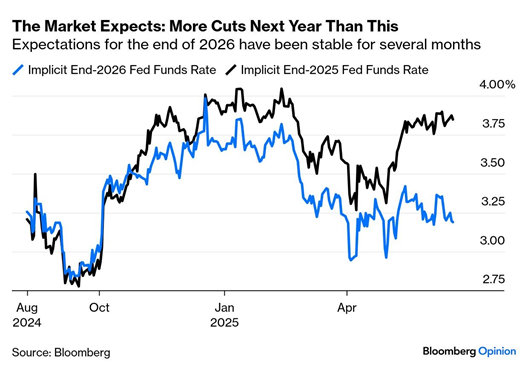

According to Bloomberg’s World Interest Rate Probabilities function, markets anticipate the fed funds rate to fall to between 3.0% and 3.25% by end-2025 – implying more rate cuts than the Federal Reserve’s own projections suggest. This divergence points to greater market concern about future growth. The Fed’s updated economic projections, meanwhile, reflected a marginally more negative growth outlook coupled with slightly higher inflation expectations – a mildly “stagflationary” shift. Source: Bloomberg.

As always, we appreciate your support and value your trust in LNKD Investment Managers.