In a meeting of the G-20’s finance ministers and central bank governors on Saturday, the group advocated for a tax plan that would cover how multinational enterprises reallocated profits and the rollout of a global minimum tax. The plan would call for a 15% global minimum corporate tax, in an effort to stop multinational corporations taking advantage of lower tax countries. Large companies such as Apple and Microsoft would be taxed based on partially where they sell their products and services and not where their headquarters are situated. The leaders are aiming to get the plan approved at a G-20 summit in October this year.

U.S. President Joe Biden signed an executive order on Friday which is aimed to tackle anticompetitive practices. The president is calling for fairer competition amongst U.S. companies in various sectors, from technology to healthcare. The order contains 72 initiatives that will counter practices that have driven up prices and disadvantaged workers.

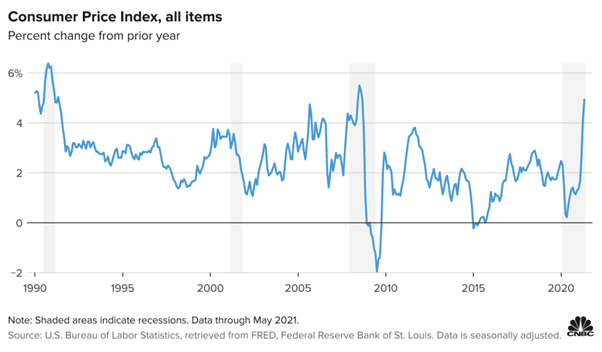

Moves in the U.S. yield this week drove market attitude, with investors interpreting falling 10 year treasury note yields first as an opportunity for risk assets but later in the week, as a possible warning sign of slowing economic growth. The reasons being mentioned in the market for the drop vary from fears of the Delta variant spreading to inflation peaking in the near term. Continuing with the topic of inflation, the Federal Open Market Committee’s June meeting resulted in member’s highlighting that tapering bond buying was going to be implemented earlier than anticipated as inflation had run hotter than members expected. Nonetheless, they maintain the argument for inflation to be transitory.

China’s central bank this week made a surprise move and lowered its reserve requirement ratio, the amount of cash banks must hold in the central bank’s reserve, on banks by 0.5%. Approximately $150 billion in long-term liquidity is expected to be released into the market as a result. This move is intended to make more liquidity available to banks in order to boost lending to businesses while supporting the real economy. Concerns still remain over China’s stock market however, as the nation’s cybersecurity crackdown continues with their focus remaining on company data risks, including how tech companies collect and store their consumer data.

Big Tech was also a theme present in Honk Kong this week. Facebook, Twitter, and Google privately warned Hong Kong’s government that if they proceed with planned changes to data protection laws, they could stop offering their services in the city, Dow Jones reports.

Japan found themselves in a fourth Covid-19 state of emergency this week as the spread of virus picked up pace, forcing the government to make the move. Following this move, Tokyo’s Olympic spectators were banned from watching the events, meaning the multi-sport event is now set to take place with no fans.

The U.K. announced plans this week to end social distancing and capacity limits at venues in England from July 19, saying that people must learn to live with coronavirus. Britons who are fully vaccinated will get more freedom to travel abroad starting 19 July. Covid-19 cases continue to rise in the nation, but hospitalizations remain low thanks to vaccinations.

The European Central Bank (ECB) set a new inflation target on Thursday and put a spotlight on their future role in the fight against climate change. The ECB set their inflation target to 2% from their previous target of “below but close to 2%”, indicating a more flexible policy framework, much like the Fed’s structure they implemented a year ago. This means that the Union’s loose policy outlook is here to stay longer.

U.S indices mostly managed slight gains after negative moves earlier in the week. The Dow Jones (0.24%), the S&P 500 (0.40%) and the Nasdaq (0.43%) just outperformed most their international peers, avoiding ending the week in the red. The Euro Stoxx 50 (-0.40%), FTSE 100 (-0.02%) and Nikkei 225 (-2.93%) all ended the week down. The Shanghai (0.15%) index manged to end the week in the green. Gold (1.17%) saw a slight rally, while brent crude (-0.62%) dipped as confusion remains over OPEC’s disagreement.

Market Moves of the Week:

In South Africa, Former President Jacob Zuma turned himself over to the police on Thursday to begin serving a 15-month prison term. Zuma handed himself over to authorities to obey the country’s highest court, the Constitutional Court, that he should serve a prison term for contempt. Twenty eight people were arrested and a highway was closed in KwaZulu-Natal, Zuma’s home province, as protests erupted following the arrest. On Friday, Zuma lost a bid to overturn his arrest, yet another legal challenge will be heard on Monday. Zuma was not the only ANC member to lose a court bid this week, Ace Magashule’s bid to have his suspension set aside was rejected by the high court on Friday too.

The Government has finally made a public pay offer that the trade unions are considering. Public servants are being offered a revised wage offer that amounts to a 1.5% increase plus a R1000 cash allowance, resulting in an effective 11.7% increase for the lowest paid public servants.

The current alcohol ban is predicted to cost the alcohol industry R6.1 billion in lost retail sales and the extension of the current lockdown remains a key threat for the industry. Premier David Makhura has stated that Gauteng is nearing the peak of its Covid-19 infections during the third wave, meaning that cases may be likely to decline soon.

The JSE All Share Index ended the week up by 0.09%. The rand strengthened to end the week at R14.17 to the U.S. Dollar.

Chart of the Week:

European policymakers agreed to raise their inflation target to 2.0% and allow room for an overshoot when needed, which would give more room for ultra-loose monetary policy for longer. The decision is part of the biggest overhaul in ECB monetary policy in two decades.

Whilst volatility is likely to continue amid current market uncertainty over the coronavirus pandemic, our message to all investors remains the same – stay calm in making decisions that are aligned with your long-term goals, not current market conditions. In any market environment, we strongly believe in the importance of having a portfolio that contains a variety of asset classes, including stocks and bonds, balanced in a way that reflects the investors risk tolerance and investment timeline.

As always, we appreciate your support and value your trust in LNKD Investment Managers..

The information included above as well as individual companies and/or securities mentioned should not be construed as investment advice, a recommendation to buy or sell or an indication of trading intent on behalf of any LNKD product. LNKD Investment Managers is an authorised financial services provider (FSP 51257).