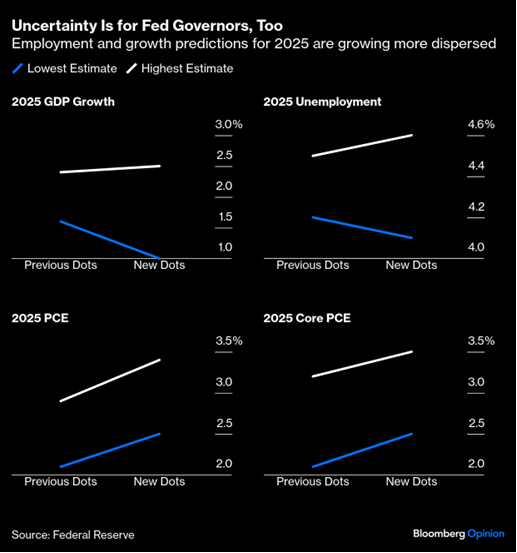

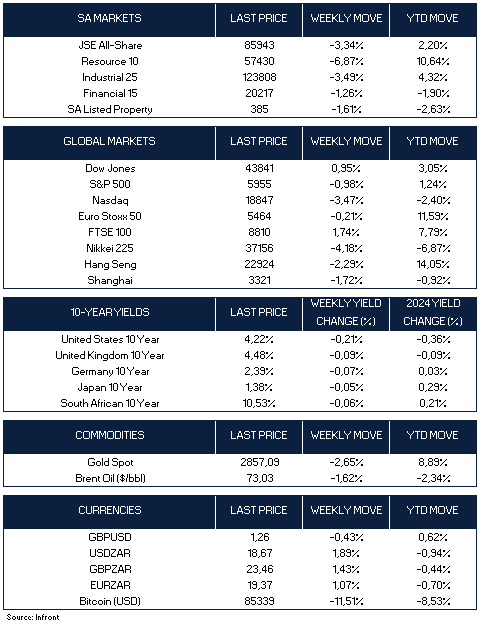

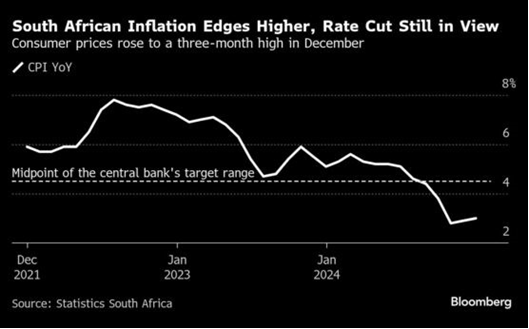

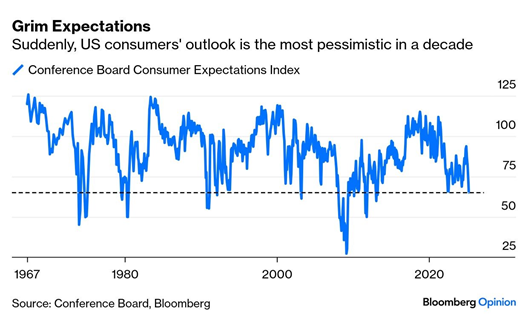

The U.S. Conference Board’s consumer confidence index dropped to 92.9 in March from 100.1 in February, marking its fourth consecutive decline. The expectations index fell 9.6 points to 65.2, its lowest in 12 years, staying below the recession-warning threshold of 80 for a second month. The report noted fading optimism about future income, reflecting growing economic and labour market concerns.

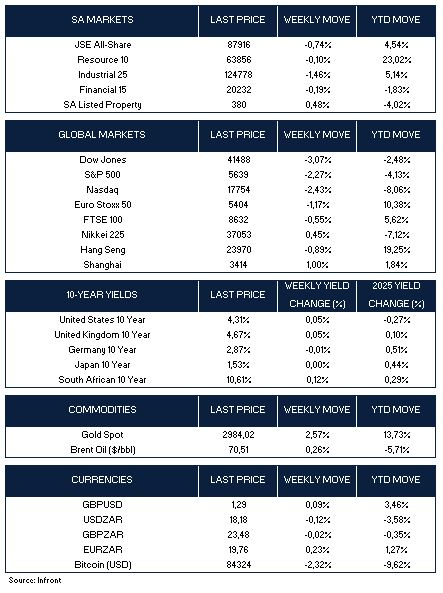

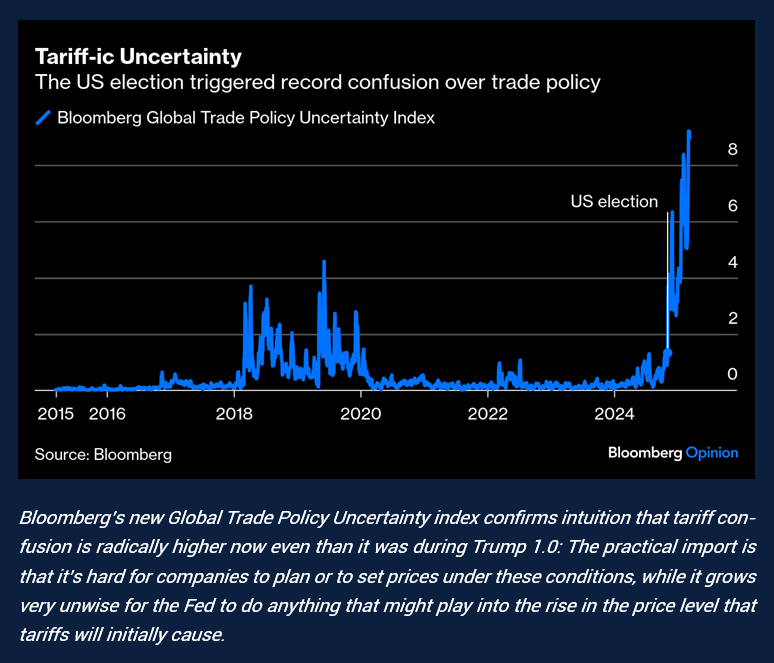

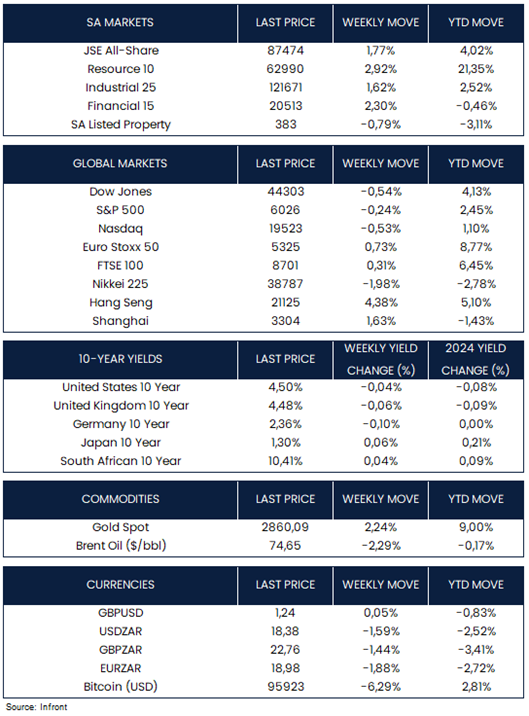

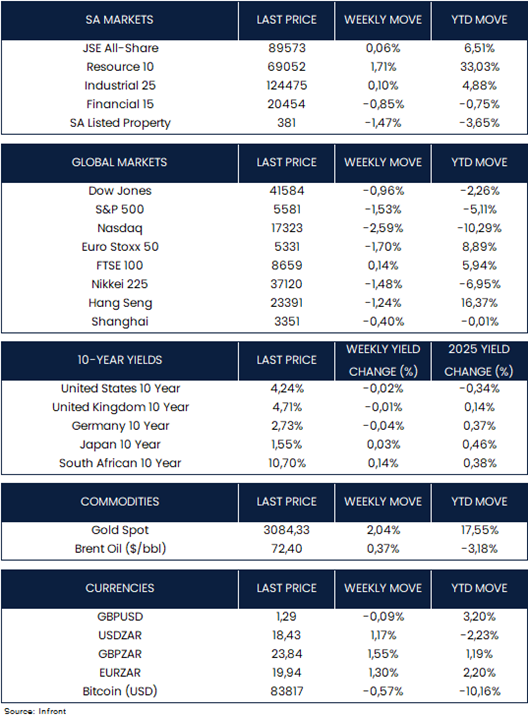

U.S. stock indexes fell over the week, weighed down by declines in the technology and communication services sectors, while value stocks outperformed growth for a sixth straight week. Markets started with cautious optimism, but sentiment shifted after new tariff announcements on Wednesday, including a 25% levy on non-U.S.-made cars, effective April 3.

Adding pressure, the Bureau of Economic Analysis reported core PCE inflation rose 0.4% in February (up from January’s 0.3% reading), with annual inflation at 2.8%, exceeding the Fed’s 2% target. Sluggish consumer spending and inflation fears contributed to a market selloff, pushing stocks lower into the week’s close. The Dow Jones (-0.96% w/w) faired best, while the S&P 500 (-1.53%) and Nasdaq (-2.59%) experienced steeper declines.

The Euro Stoxx 50 Index closed -1.70% over the week as Trump’s fresh auto tariffs hurt sentiment. The blanket application was the worst-case scenario for Europe, as there had been hopes that some countries might be granted an exemption. This marked a disappointing week for European markets, which had begun positively, buoyed by favourable economic updates and geopolitical news.

In the UK, British Chancellor Rachel Reeves presented the annual Spring Statement, announcing additional spending cuts. The Office for Budget Responsibility (OBR) lowered its UK economic growth forecast for 2025 to 1%, also predicting higher unemployment and inflation this year. However, the OBR raised its growth projections for 2026-2029. On a positive note, UK inflation eased to 2.8% in February from 3% in January, keeping the prospect of a May interest rate cut alive. The FTSE 100 ended the week 0.14% higher.

Japan’s stock market declined over the week, with the Nikkei 225 Index dropping 1.48%. Japan’s Prime Minister Shigeru Ishiba called the impact of the U.S. auto tariff on Japan’s key auto industry and economy “significant,” noting that autos make up about one-third of Japan’s U.S. exports. He emphasized the need for appropriate responses, with all options considered. Japan is pushing for an exemption from the tariff through diplomatic efforts, including increased investments and energy purchases. Elsewhere in Asia, China’s Shanghai Index (-0.40%) ended the week little changed amid a light economic calendar.

On the commodity front, “safe haven” Gold (+2.04% w/w) hit all-time highs on Friday ($3,086) after the release of US PCE data. Brent oil ended the week up 0.37% for its third weekly gain.

Market Moves of the Week:

The South African (SA) government is establishing a Private Sector Participation (PSP) unit to attract investment in ports and rail, mirroring the success of the independent power producers’ office. Transport Minister Barbara Creecy said a deal with the Development Bank of Southern Africa (DBSA) and National Treasury is in its final stages, with the DBSA set to host the unit.

SA retail confidence fell from 54% to 50% in Q1 2025, according to the Bureau for Economic Research (BER). Despite the dip, confidence remains above the long-term average, with half of retailers satisfied with business conditions. The BER noted improving sentiment in the motor trade sector, especially among new vehicle dealers, as a positive sign for consumer health.

Foreign investors offloaded South African equities at the fastest rate in over a year during Q4 2024, favouring the country’s bonds instead. This shift contributed to a 26% decline in portfolio inflows, which fell to 33.4 billion rand ($1.8 billion) compared to the previous quarter, according to the South African Reserve Bank’s Quarterly Bulletin released on Thursday.

On the political front, News24 reported Friday that the ANC rejected the DA’s request for a deal on jointly managing economic policy. The DA had reportedly tied its budget support to securing such an agreement.

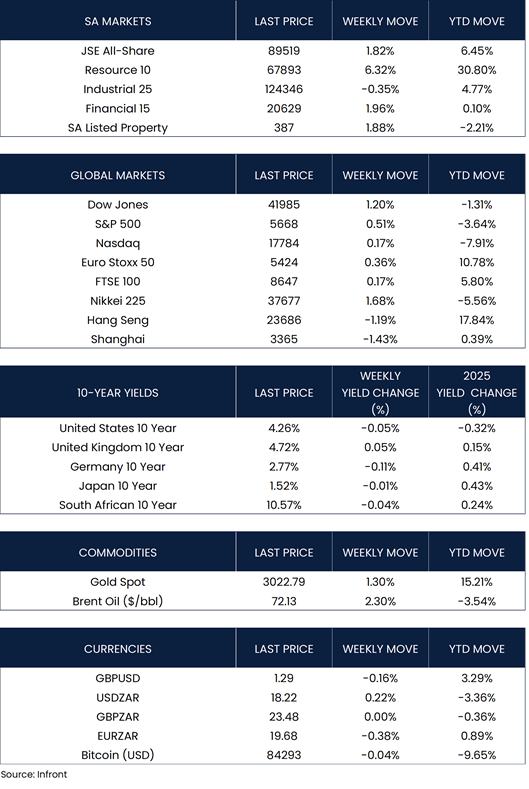

The All-Share Index edged higher on the week (+0.06%), driven by gains in Resources (+1.71%). The local currency weakened against the U.S. dollar, moving to R18.43/$ from last week’s R18.22/$ level. SA’s 10-year government bond yield rose 0.14% over the week.

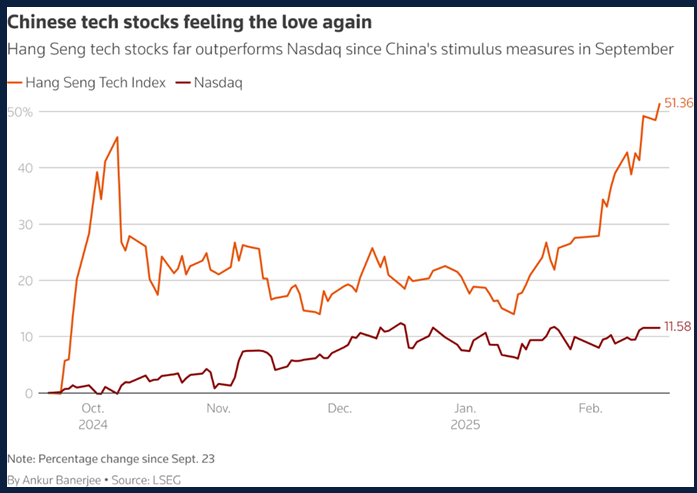

Chart of the Week:

The latest survey of consumer sentiment by the Conference Board found expectations dropping to their lowest level in a decade (a period that includes both the pandemic and the inflation spike): Source: Bloomberg.

As always, we appreciate your support and value your trust in LNKD Investment Managers.