Brent crude rallied on Friday, settling 7.0 % higher at USD 74.23 per barrel after Israel and Iran exchanged air strikes. Intraday, the benchmark briefly touched USD 78.50, its highest level since 27 January. Although no oil facilities were hit, investors remain sensitive to the risk of further escalation, particularly given Iran’s strategic position near the Strait of Hormuz, through which roughly 20 % of global oil supply transits. Iran’s April output of 3.3 million barrels per day underscores the region’s systemic importance. The International Energy Agency stated it retains 1.2 billion barrels of emergency reserves and is prepared to act if required. Even after Friday’s surge, Brent remains more than 10 % below its level a year ago and well off the peaks above USD 100 recorded in early 2022.

U.S. Treasuries generated positive returns through Thursday as yields declined in response to the week’s economic data releases, particularly the softer-than-expected CPI report on Wednesday, although Treasuries across most maturities gave back some gains on Friday morning following Israel’s attack on Iran.

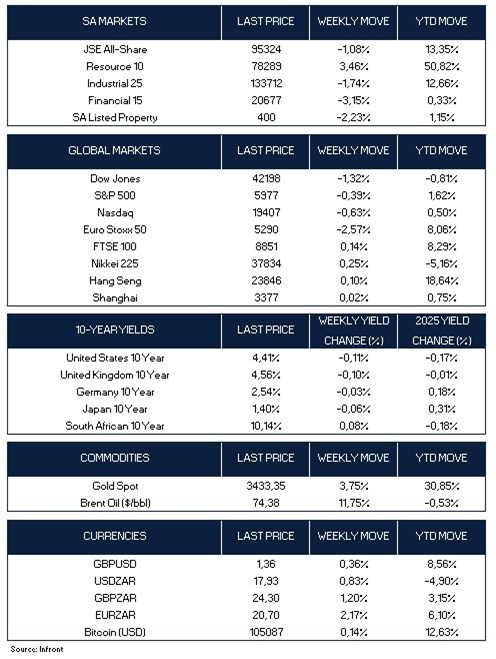

On the equities front, US stocks ended the week lower amid escalating tensions in the Middle East. The Dow Jones Industrial Average fell 1.3 % on the week, turning negative year‑to‑date, while the S&P 500 and Nasdaq Composite retreated more modestly and remain in positive territory.

The US May consumer‑price data surprised on the downside. Headline CPI rose 0.1 % m/m (consensus: 0.3 %) and 2.4 % y/y, while core CPI held steady at 2.8 % y/y. The first full month of new import tariffs had only a marginal impact on core‑goods prices. Consequently, market expectations for Federal Reserve policy were little changed.

In Europe, the STOXX Europe 50 Index lost 2.6 % as investors grappled with geopolitical risks and uncertainty over U.S. trade policy.

The UK economy shrunk in April by 0.3% m/m, the sharpest decline since October 2023, driven by weakness in services and production. Unemployment rose to 4.6 %, a four‑year high. The FTSE 100 ended the week broadly flat.

Japanese equities were mixed over the week with the benchmark Nikkei 225 index gaining 0.25% amid escalating geopolitical risks and an uptick in trade-related concerns. Safe‑haven demand supported the yen, which strengthened to the high‑JPY 143 range versus the U.S. dollar.

Mainland Chinese stock markets ended flat as the latest inflation snapshot of deflationary pressures persisted, while in Hong Kong, the Hang Seng Index edged up 0.1%.

China’s CPI declined for a fourth consecutive month in May, underscoring weak domestic demand amid the protracted property downturn. Producer prices dropped for a 32nd straight month, marking the steepest fall in almost two years. While the recent tariff détente with the United States has improved the near‑term growth outlook, economists remain cautious on the trajectory of consumer prices.

Market Moves of the Week:

South Africa has successfully completed all 22 action items required by the Financial Action Task Force (FATF), the international body that greylisted the country in February 2023. This development paves the way for a potential removal from the greylist during the FATF’s next review in October.

The achievement reflects a marked improvement since the 2021 FATF assessment, where South Africa was found significantly non-compliant in areas of financial crime enforcement and regulatory oversight. The greylisting has since subjected the local financial sector to heightened international scrutiny, impacting investor sentiment, raising operational costs, and elevating the risk of capital outflows.

The FTSE/JSE All Share Index declined 1.8% on Friday, driven primarily by losses in the Financial 15 Index, which fell more than 2.7% on the day. However, on a weekly basis, the All Share Index posted a more moderate decline of just over 1.0%.

Offsetting broader weakness, gold mining stocks rallied strongly, reaching record highs as the gold price surged above USD 3,440/oz—approaching a historical peak—following reports of Israeli air strikes on Iranian nuclear and military infrastructure.

The rand depreciated against a stronger U.S. dollar on Friday, in response to escalating geopolitical tensions. Persistent rand weakness, coupled with a sustained rise in Brent crude oil prices, poses a challenge to the South African Reserve Bank (SARB), which remains focused on containing inflationary pressures. Should these trends continue, consumers can expect higher domestic fuel prices in July and possibly beyond.

Looking ahead, upcoming consumer inflation and retail sales data, due next week, may provide further insight into the SARB’s policy stance, although the next interest rate decision is scheduled for late July.

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.