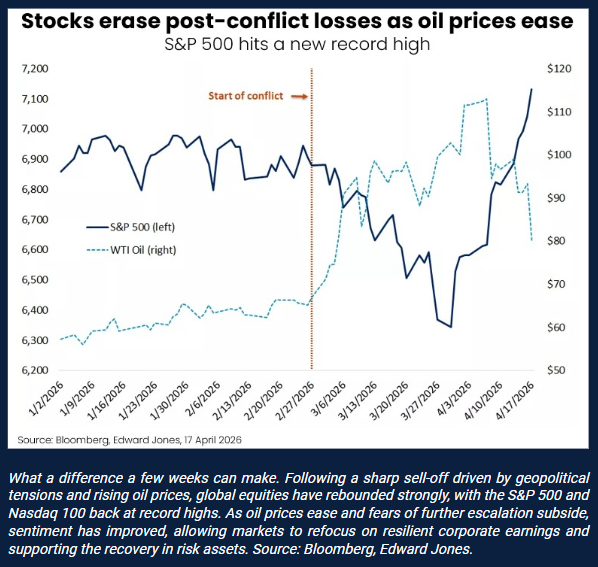

What a difference a few weeks can make. Markets have shifted rapidly from pricing in geopolitical shock and stagflation risk to a more constructive backdrop, with global equities rebounding sharply and major indices pushing back toward record highs. This recovery has been driven by easing oil prices, stabilising bond yields, and a reduction in immediate geopolitical risk. Importantly, corporate earnings have been resilient, continuing to provide a strong foundation for markets.

Developments in the Middle East remain central to market direction. A ceasefire agreement and signs of progress toward broader diplomatic engagement have helped ease immediate concerns around global energy supply, contributing to a pullback in oil prices. That said, the situation remains fluid, with earlier tensions briefly pushing Brent crude back toward $100 per barrel. The International Energy Agency estimates that around 13 million barrels per day of supply have been disrupted, highlighting the scale of the shock and the potential for further volatility should tensions re-escalate.

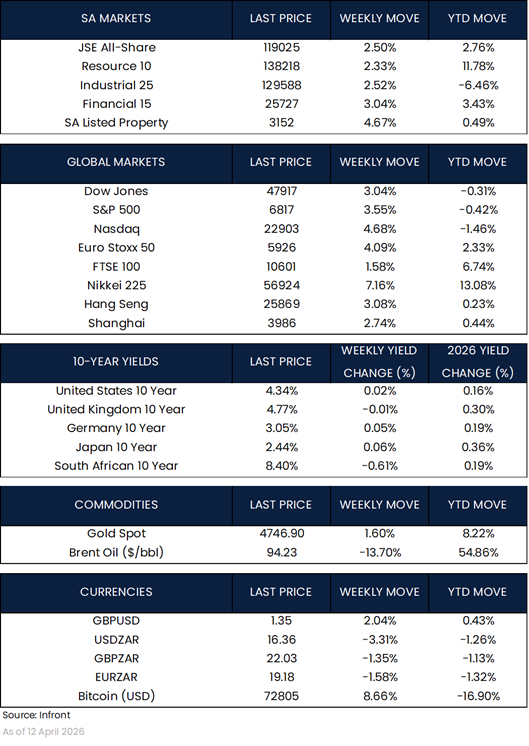

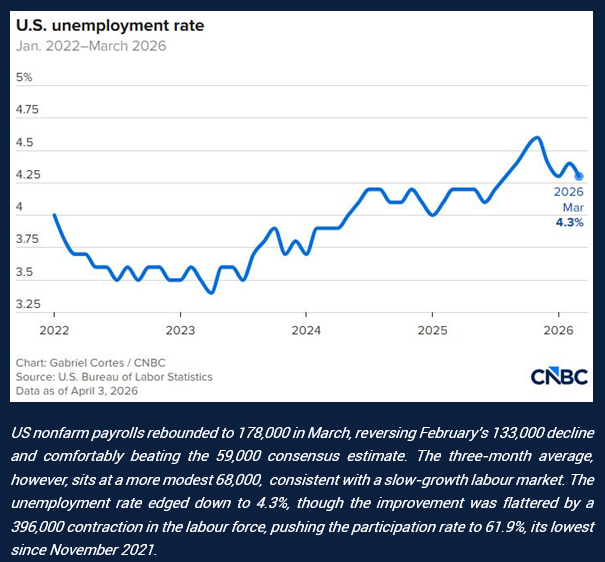

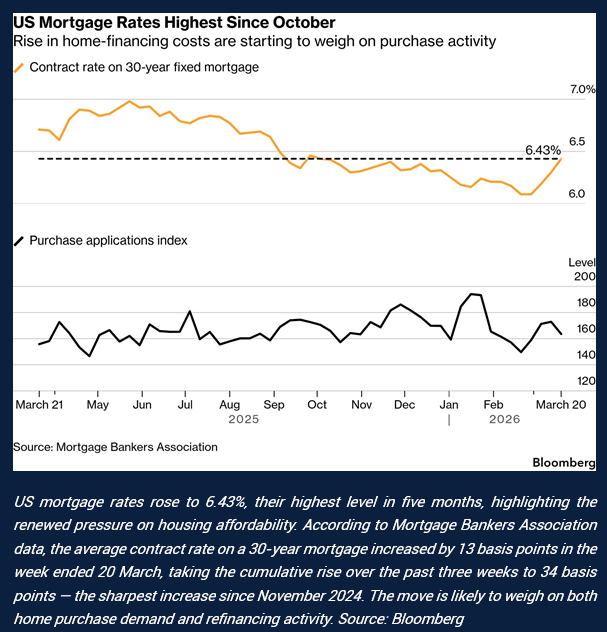

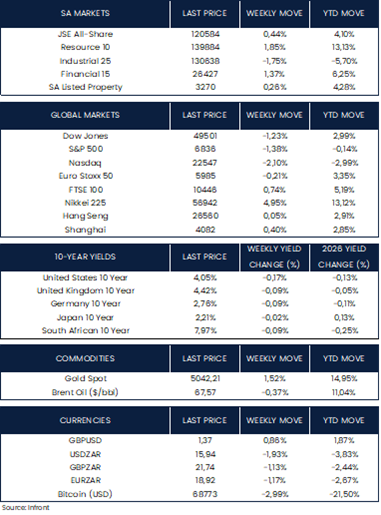

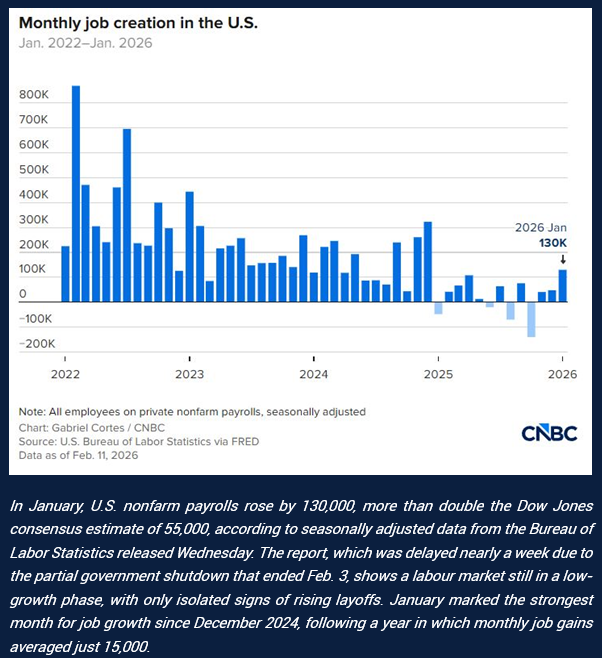

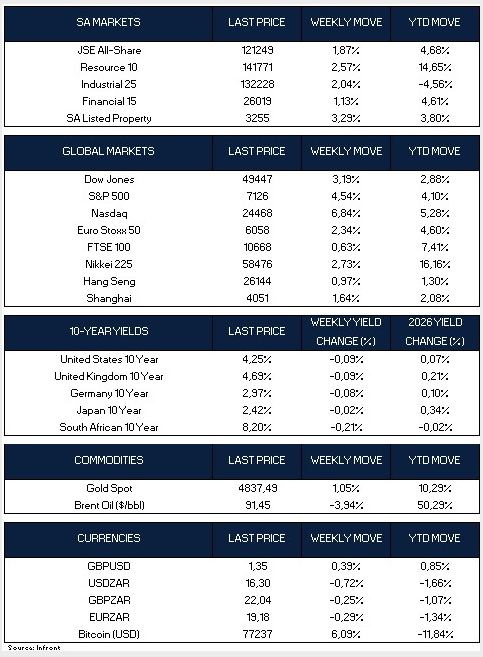

Against this backdrop, U.S. equity markets rebounded strongly, with the Dow Jones rising 3.19%, the S&P 500 gaining 4.54%, and the Nasdaq outperforming at 6.84%. The rally has been supported by a solid start to earnings season, particularly within the banking sector, alongside broadly stable economic data. Producer price inflation came in softer than expected at 0.5% month-on-month, while jobless claims declined to 207,000, pointing to a resilient labour market. Manufacturing indicators also improved, suggesting a pickup in activity. However, some areas remain under pressure, with industrial production declining 0.5% month-on-month and existing home sales falling 3.6%, highlighting ongoing weakness in housing.

In Europe and the UK, markets were also stronger this week, with the Euro Stoxx 50 rising 2.34% and the FTSE 100 advancing 0.63%. Economic data was mixed but generally supportive. UK GDP surprised to the upside, growing 0.5% month-on-month in February, while retail sales rose 3.1% year-on-year. Industrial production also improved modestly, although manufacturing output declined slightly. In the eurozone, industrial production returned to growth, rising 0.4% month-on-month. Inflation remains a key consideration, with headline inflation around 2.5% year-on-year, driven in part by energy prices. While underlying inflation pressures are gradually easing, risks remain tilted to the upside, and central banks continue to adopt a cautious, wait-and-see approach.

In Asia, performance remained positive but more moderate, led by Japan’s Nikkei 225 (+2.73%), while the Hang Seng (+0.97%) and Shanghai Composite (+1.64%) posted more modest gains. In Japan, policy expectations have softened, with the Bank of Japan maintaining a cautious stance amid uncertainty around energy prices and growth. The 10-year government bond yield remained around 2.41%, while the yen traded near 159 to the U.S. dollar. Business sentiment weakened notably, with manufacturing confidence recording its sharpest decline in over three years.

China’s economy continues to show signs of stabilisation, with first-quarter GDP expanding 5.0% year-on-year and 1.3% quarter-on-quarter. However, the underlying picture remains uneven. Industrial production rose 5.7% year-on-year, but retail sales slowed to 1.7%, pointing to weaker consumer demand. Fixed asset investment grew 1.7%, while property investment declined sharply by over 11%, underscoring ongoing pressure in the real estate sector.

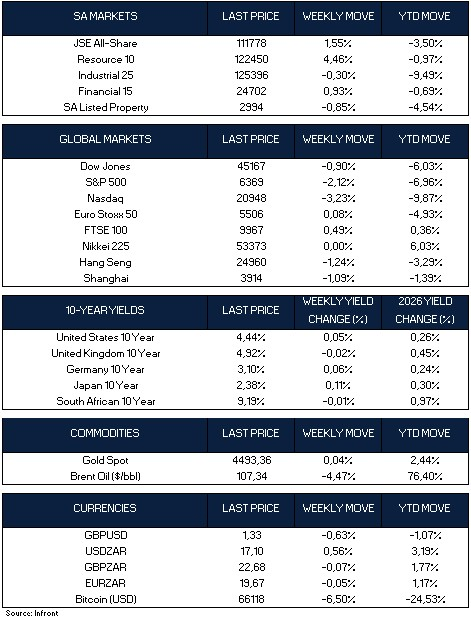

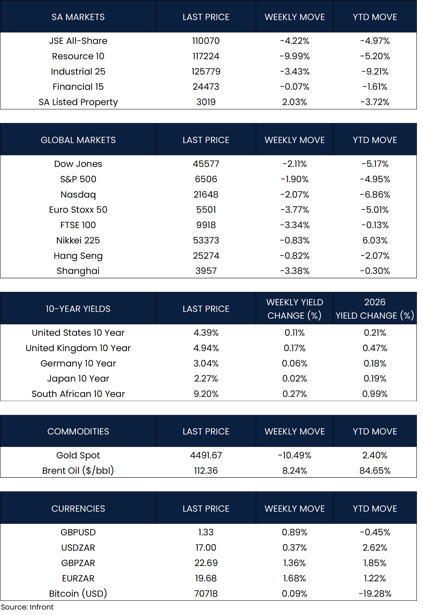

Market Moves of the Week:

Locally, the story remains one of gradual stabilisation. Mining production surprised to the upside, rising 2.3% month-on-month and 9.7% year-on-year, supporting the growth outlook. Eskom’s three-year wage agreement provides further operational certainty, building on improved electricity supply conditions. While these developments are encouraging, structural challenges remain, particularly around the pace at which investment commitments translate into real economic activity.

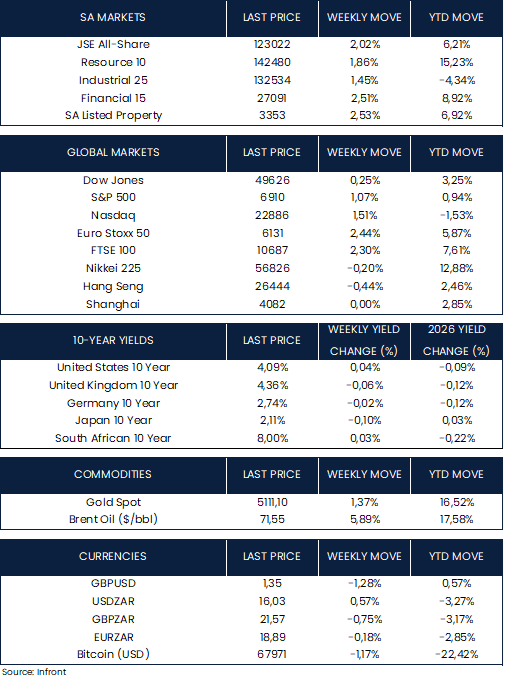

South African markets ended the week firmer, with the JSE All Share Index gaining 1.87%. Resources led the advance (+2.57%), while industrials (+2.04%) and financials (+1.13%) also contributed positively. Listed property was a standout performer, rising 3.29% on the week. The rand strengthened modestly to around R16.30 against the U.S. dollar, while the South African 10-year government bond yield declined by 21 basis points to 8.20%, reflecting improved sentiment toward local fixed income.

Overall, markets have moved quickly from pricing in disruption to refocusing on fundamentals. While geopolitical developments remain a key near-term driver, the resilience of corporate earnings and signs of economic stabilisation continue to provide support. Periods of volatility are likely to persist, but the underlying picture remains constructive, reinforcing the importance of maintaining a diversified, long-term investment approach.

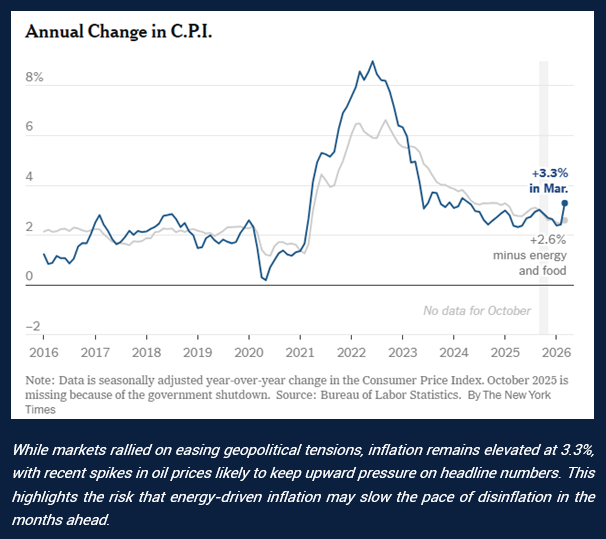

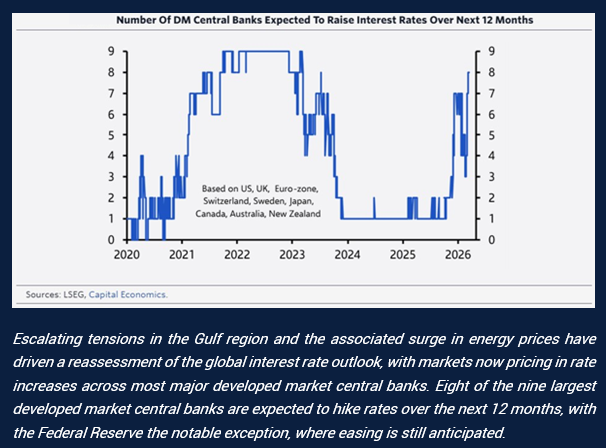

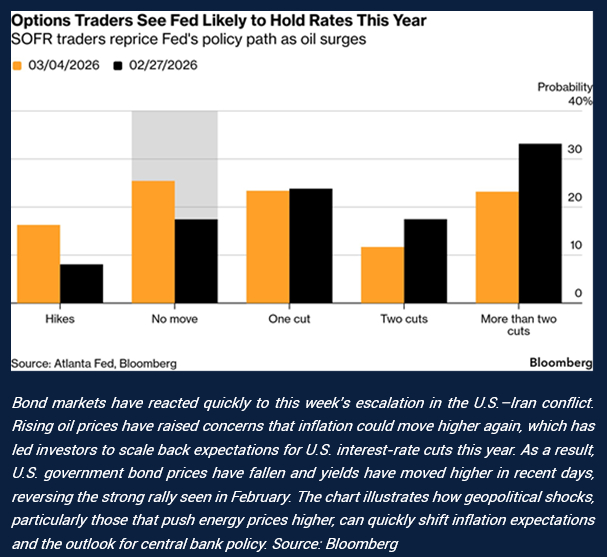

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.