The United States and China have agreed to a 90-day suspension of recently imposed tariff measures as part of efforts to reset bilateral trade negotiations. Under the terms, the effective U.S. tariff rate on the bulk of Chinese imports will be scaled back from a peak of 145% to 30%, while China will reduce its applied tariffs on U.S. goods from 125% to 10%. The accord, reached during bilateral consultations in Geneva, also covers the withdrawal of recent non-tariff barriers, marking a temporary de-escalation in a dispute that has disrupted trade flows and heightened geopolitical risk.

The U.S. Bureau of Labor Statistics reported that inflation eased in April, with the Consumer Price Index rising 0.2% month-on-month and 2.3% year-on-year—the slowest annual pace in over four years. Cooler food prices helped offset persistent rental inflation, while core CPI, which excludes food and energy, also increased 0.2% for the month, with an annual rate of 2.8%.

Separately, the Bureau released data showing that producer prices unexpectedly declined 0.5% in April after a revised flat reading in March. This drop was led by the largest fall in service costs since 2009, reflecting weaker demand for air travel and hotel stays. The report also noted narrower profit margins, suggesting companies are absorbing some of the cost pressures from higher tariffs.

U.S. retail sales growth slowed sharply in April, with headline sales up just 0.1% after a 1.7% surge in March. The fading boost from front-loaded auto purchases ahead of tariffs weighed on momentum, while broader consumer spending softened amid rising economic uncertainty. Core retail sales, which align closely with the consumption component of GDP, fell 0.2%, signaling a more cautious consumer heading into the second quarter.

Britain’s economy expanded 0.7% in the first quarter, exceeding expectations and accelerating from 0.1% growth in the previous quarter. Growth was driven by strong contributions from the services sector, fixed investment, and net exports, demonstrating resilience ahead of the U.S. tariffs implemented on 2 April. Meanwhile, the UK labour market showed signs of softening, with the Office for National Statistics reporting the unemployment rate rising to 4.5% from 4.4% in the three months through March.

Industrial production in the euro area surged 2.6% in March, signaling a potential recovery from a two-year contraction in the sector. The expansion was primarily driven by robust gains in capital goods and durable consumer goods, surpassing February’s 1.1% increase.

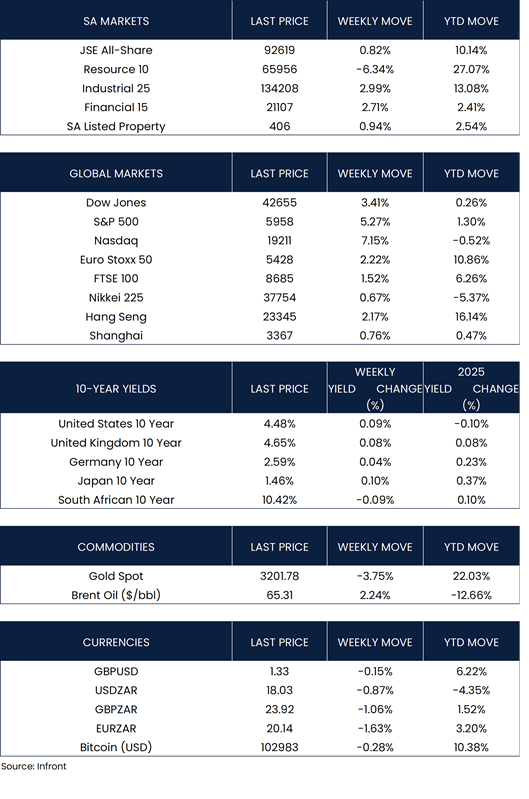

Global equity markets rallied over the week, buoyed by easing trade tensions between the U.S. and China. In the U.S., the Nasdaq Composite led with a 7.15% increase, while the S&P 500 and Dow Jones Industrial Average rose 5.27% and 3.41%, respectively.

European markets also advanced, with the STOXX Europe 50 up 2.22% and the UK’s FTSE 100 gaining 1.52% in local currency terms. In Asia, the Nikkei 225 added 0.67%, while the Shanghai Composite and Hang Seng Index rose 0.76% and 2.17%, respectively.

Market Moves of the Week:

South Africa’s official unemployment rate rose to 32.9% in Q1 2025, up from 31.9% in the previous quarter, according to Statistics South Africa. Employment fell notably in the formal sector, particularly in trade, construction, and social services. However, there were modest gains in the informal sector and in industries such as transport, finance, and utilities.

Deputy Finance Minister David Masondo recently indicated that the Treasury and the South African Reserve Bank are finalising revisions to the country’s inflation-targeting framework, with an announcement expected soon. SARB Governor Lesetja Kganyago has advocated for tightening the inflation target to a single point around 3%, in line with emerging market peers, to better anchor inflation expectations. However, persistent structural inflationary pressures—particularly from administered prices linked to state-owned entities—pose significant challenges. This suggests that interest rates may remain elevated for longer, potentially constraining GDP growth and employment recovery in the near to medium term.

Mirroring global trends, the JSE All-Share Index increased by 0.82% over the week, supported by a 2.99% gain in the industrial sector. The financial and property sectors also advanced by 2.71% and 0.94%, respectively. Conversely, the resources sector declined by 6.34%, weighing on overall market performance. By Friday’s close, the rand appreciated 0.87% against the U.S. dollar, trading at R18.03/$.

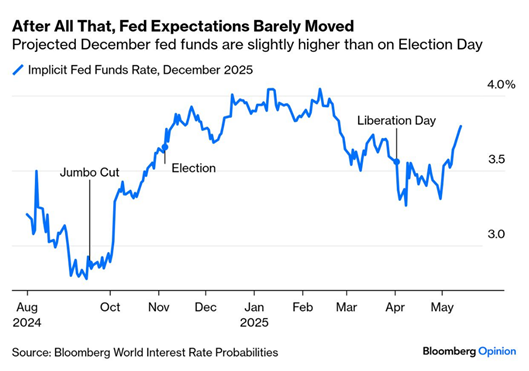

Chart of the Week:

US inflation eased for the third consecutive month in April, despite a peak in import tariffs. While lower inflation typically signals room for Fed rate cuts, rising optimism about avoiding a recession has tempered expectations for monetary easing.

As always, we appreciate your support and value your trust in LNKD Investment Managers.