This week’s economic indicators and market performance signal cautious optimism, with inflation cooling in key regions and corporate earnings boosting confidence.

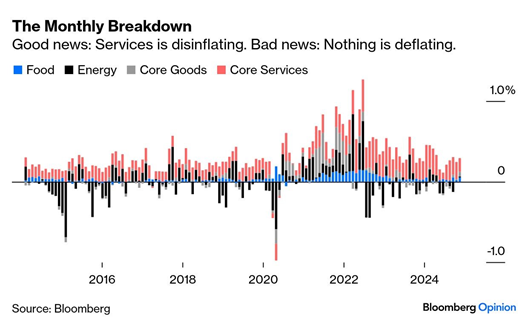

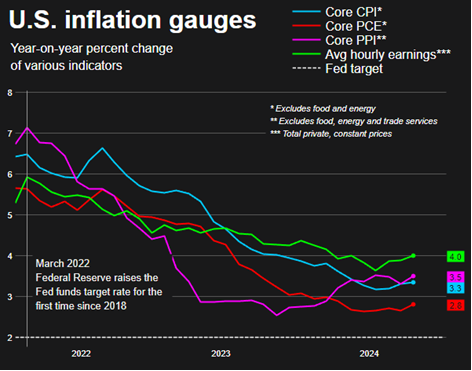

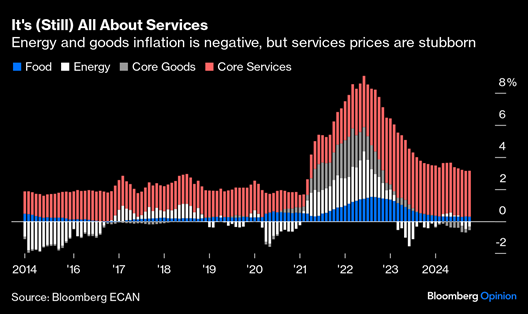

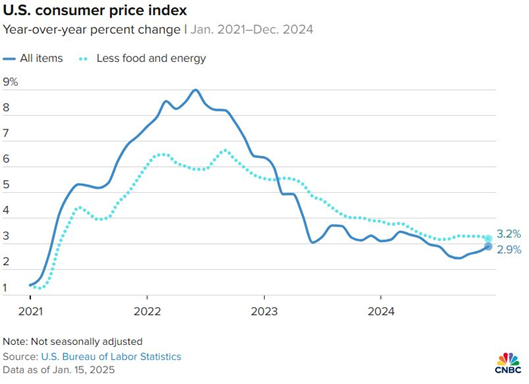

In the U.S. the consumer price index (CPI) increased by a seasonally adjusted 0.4% in December, bringing the 12-month inflation rate to 2.9%, according to the U.S. Bureau of Labor Statistics. While the headline figure indicated a slight acceleration from November, core inflation, which excludes food and energy, rose by only 0.2% in December—its smallest increase since July. Year-over-year core inflation also eased to 3.2% from 3.3% in November, falling slightly below expectations. Following the report, U.S. Treasury yields strengthened across most maturities, reflecting investor optimism.

The inflation report arrives amid heightened market sensitivity to Federal Reserve policy signals as well as concerns over tariffs and potential inflationary pressures linked to policies from President-elect Donald Trump.

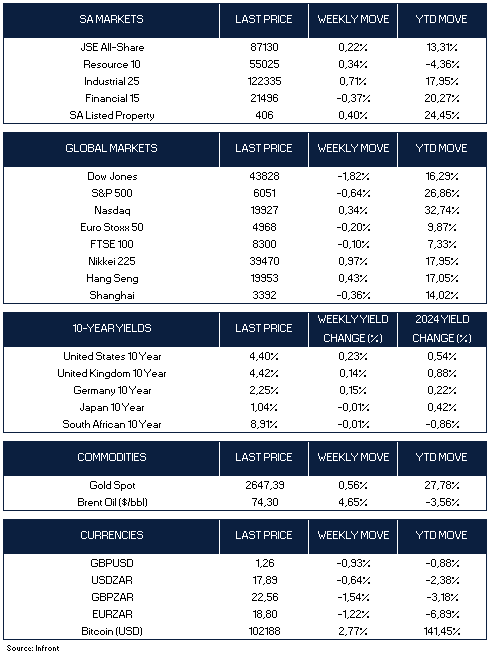

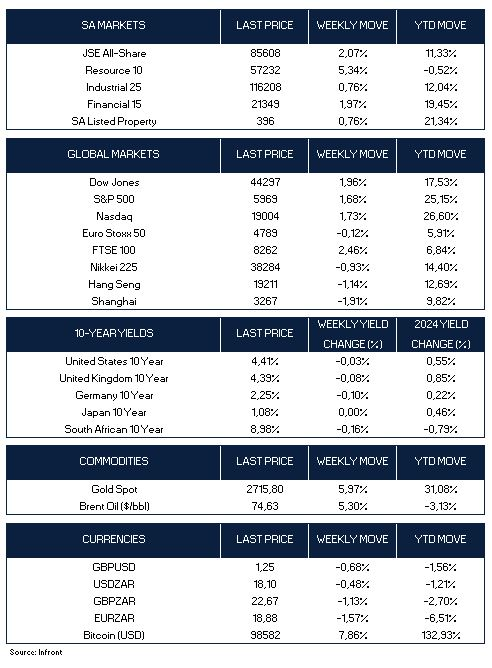

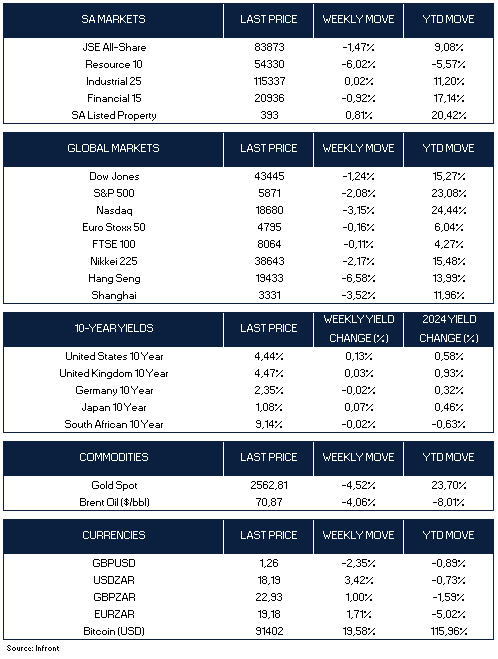

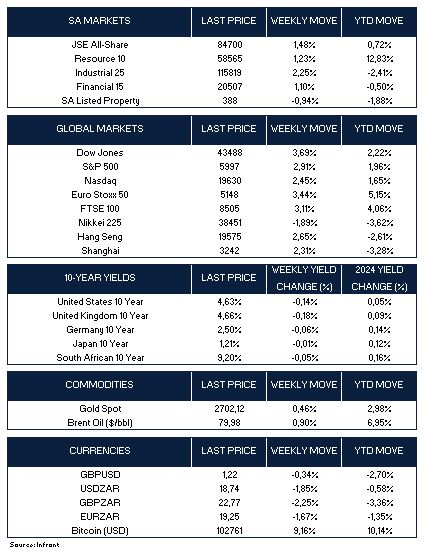

The positive inflation print as well as strong earnings reports from major banks buoyed investor sentiment this week with both the Dow Jones Industrial Average and the S&P 500 climbing 3.7% and 2.9%, respectively, marking their strongest weekly gains since the U.S. presidential election in November. The Nasdaq also posted a solid 2.5% gain.

Negotiators reached a deal on Wednesday for a ceasefire in the Gaza war between Israel and Hamas. Israel’s security cabinet approved the deal on Friday. Under the terms of the first phase of a three-phase agreement, Hamas is to release 33 hostages and Israel is to free Palestinian prisoners while the two sides attempt to negotiate a lasting truce in six weeks.

In Asia, Japanese equities faced headwinds as the Nikkei 225 Index fell 1.9% amid hawkish signals from Bank of Japan officials, heightening expectations of a potential rate hike at the upcoming policy meeting. Conversely, Chinese markets rallied with the Shanghai Composite Index gaining 2.31%, while the benchmark Hang Seng Index was up 2.73%, according to FactSet. The gains were supported by stronger-than-expected economic data. China’s GDP grew 5.4% in Q4, lifting full-year 2024 growth to 5.0% in line with official targets. Retail sales rose 3.7% year-over-year in December, while industrial output expanded 6.2%. However, consumer inflation remained subdued, and the urban unemployment rate ticked up slightly to 5.1%.

Crude oil prices rose amid new U.S. sanctions on Russian oil companies, reducing supply to China and India and pushing those countries to buy more on the open market. Brent crude ended the week up 0.9% at $79.98 per barrel. Gold prices saw marginal gains, closing at $2,702 per ounce, as lower U.S. Treasury yields increased demand for safe-haven assets.

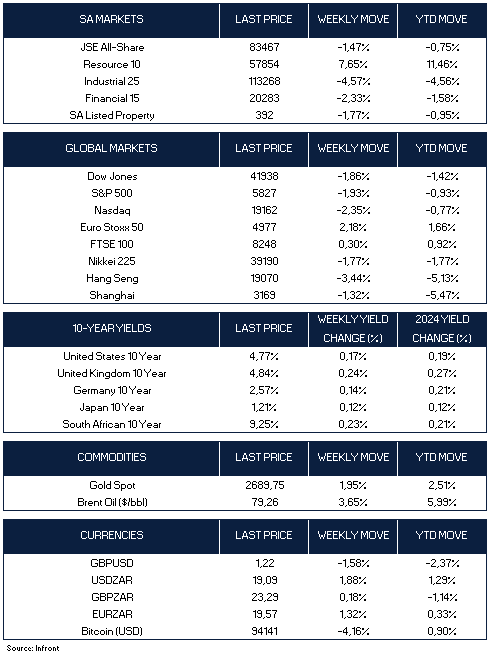

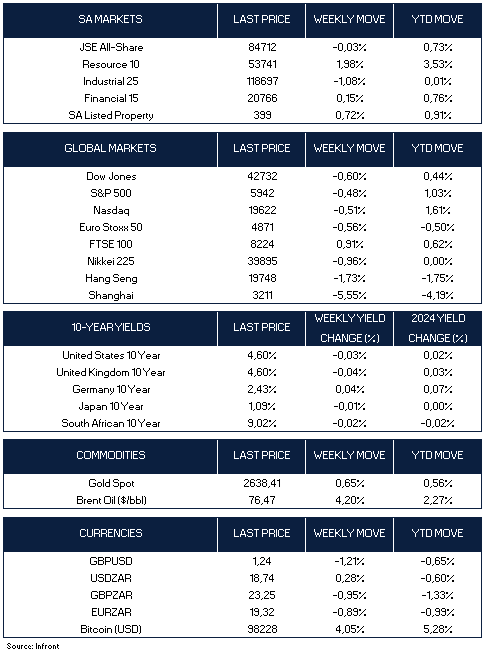

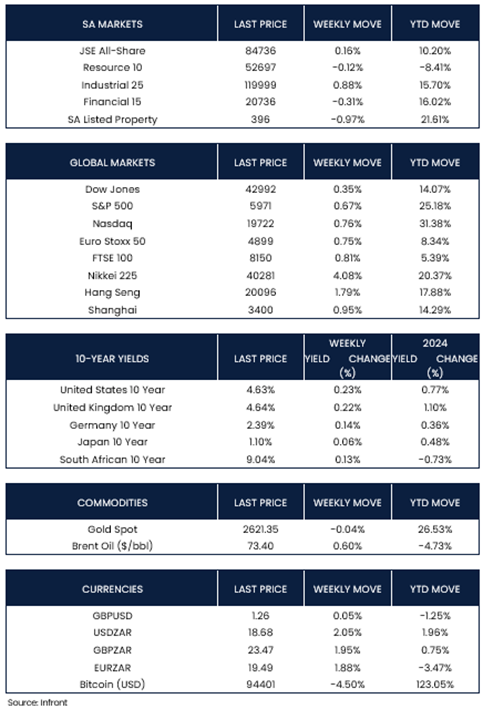

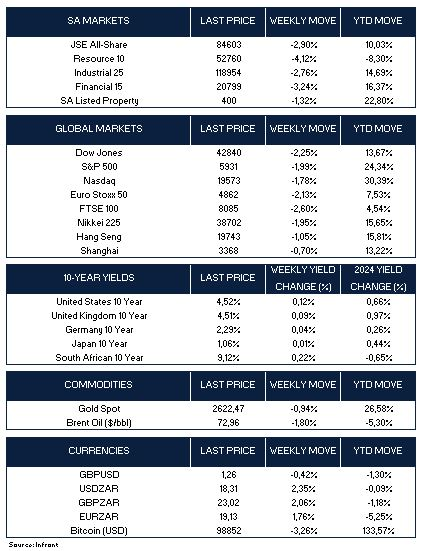

Market Moves of the Week:

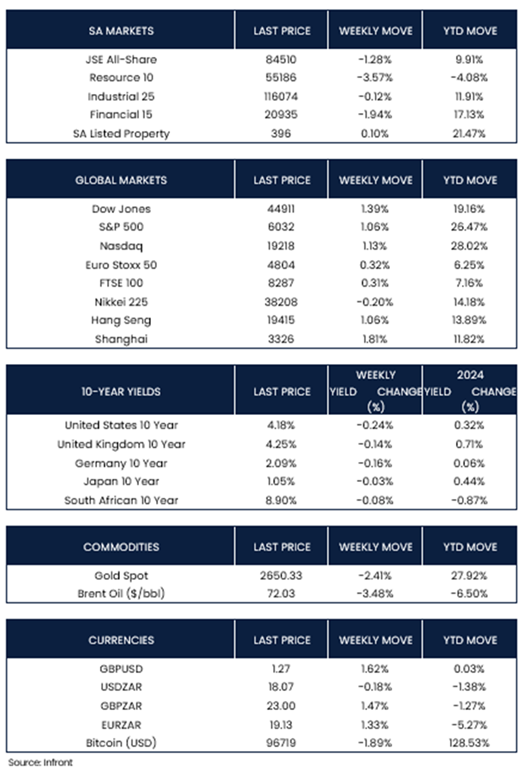

In South Africa, the number of consumers applying for loans and those falling into arrears hit a record high in the third quarter, according to data released by the National Credit Regulator on Tuesday. The report revealed 18.1 million credit applications during the quarter, marking a 3% increase from the second quarter and a nearly 50% surge since the end of 2021, when the economy began recovering from the Covid-19 pandemic. Notably, mortgage arrears climbed to 6.9% of outstanding loans, and overdue payments (one to three months late) remained elevated, reflecting financial strain on consumers.

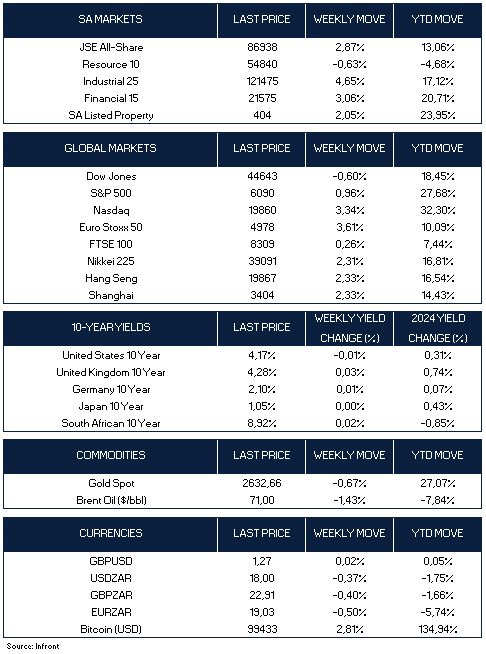

The JSE All Share Index advanced 1.48% for the week, driven by significant gains in industrial luxury goods retailer Cie Financiere Richemont S.A. Shares of the company soared 14.5% after reporting a 10.0% increase in third-quarter 2025 sales, supported by double-digit growth across the Americas, EMEA, and Japan.

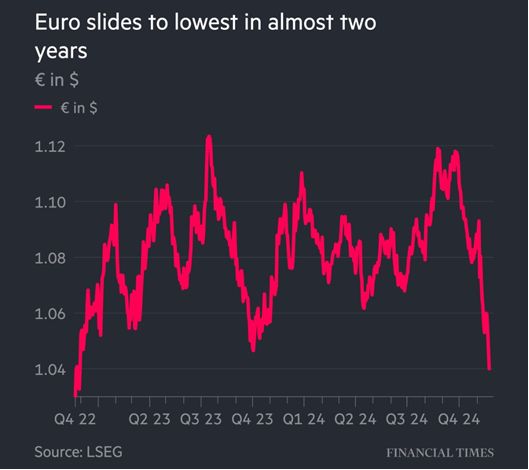

On the currency front, the rand strengthened in cautious trading on Friday, closing the week at 18.74 against the U.S. dollar, representing a weekly gain of 1.85% . Market sentiment was influenced by investor attention shifting towards the U.S. President-elect Donald Trump’s upcoming inauguration on Monday.

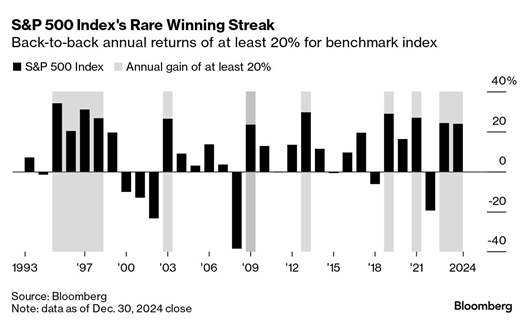

Chart of the Week:

The consumer price index increased a seasonally adjusted 0.4% on the month, putting the 12-month inflation rate at 2.9%, the Bureau of Labor Statistics reported Wednesday. However, excluding food and energy, the core CPI annual rate was 3.2%, a notch down from the month before and slightly better than the 3.3% forecast.

As always, we appreciate your support and value your trust in LNKD Investment Manager.