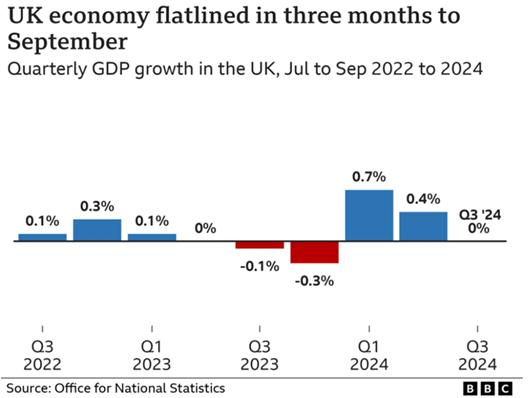

Revised figures from the UK’s Office for National Statistics revealed that the economy showed no growth in the three months to September. This marks a downgrade from the preliminary estimate of 0.1% GDP growth published earlier.

French President Emmanuel Macron has announced a new cabinet under Prime Minister François Bayrou, following the collapse of the previous government earlier this month. Bayrou is the fourth prime minister appointed within a year, as the administration grapples with challenges, including a widening fiscal deficit.

US consumer confidence unexpectedly declined in December, breaking a three-month streak of gains. The Conference Board’s index, which measures consumers’ sentiments on business and labour market conditions, fell by 8.1 points to 104.7. This was below consensus expectations, as concerns over the economic outlook and uncertainty surrounding the Trump administration’s policies weighed on sentiment.

New home sales in November fell slightly short of consensus expectations, with the Census Bureau reporting a seasonally adjusted annual rate of 664,000. Despite this, the November figure marked a significant improvement from the previous month, which had been adversely affected by hurricanes in southeast United States.

Bank of Japan Governor Kazuo Ueda stated on Wednesday that the economy is expected to move closer to sustainably achieving the central bank’s 2% inflation target next year. He indicated that further interest rate hikes may be necessary if economic conditions improve as projected. However, the timing and pace of any adjustments will depend on developments in economic activity, price trends, and financial conditions. Governor Ueda highlighted the importance of maintaining an accommodative policy stance while ensuring inflation does not exceed the 2% target.

China’s industrial profits fell 7.3% year-on-year in November, marking the fourth consecutive month of declines. However, the contraction was less steep than the 10% drop in October and the 27.1% slump in September. Meanwhile, the World Bank revised its growth forecasts for China, now expecting GDP to rise 4.9% in 2024, up from a previous 4.8% estimate. While growth for 2025 is projected to slow to 4.5%, it remains above earlier expectations of 4.1%, supported by policy easing and short-term export strength. Challenges in the property sector and subdued business confidence, however, continue to pose risks.

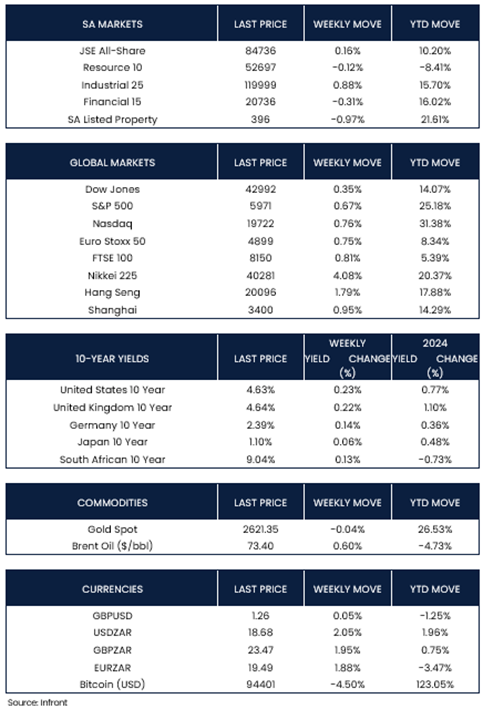

US stock indexes produced moderate gains in the final full week of the year. The Nasdaq Composite, S&P 500 Index, and Dow Jones Industrial Average all posted gains of 0.76%, 0.67%, and 0.35%, respectively. In Europe, equities edged higher during the shortened holiday trading week, with the STOXX 50 Index up 0.75% in local currency terms and the UK’s FTSE 100 Index gaining 0.81%.

Asian markets also saw positive momentum. Chinese stocks rose on optimism about potential government stimulus to bolster economic growth, with the Shanghai Composite Index climbing 0.95% and Hong Kong’s benchmark Hang Seng Index advancing 1.79%. Japanese equities recorded strong gains, as the Nikkei 225 Index surged 4.08% over the week.

Market Moves of the Week:

During the week, the JSE All-Share Index posted a modest gain of +0.16%, primarily driven by a 0.88% increase in the industrial sector. The other sectors finished the week slightly lower, with the resource, financial, and property sectors declining by -0.12%, -0.31%, and -0.97%, respectively. By the close of trading on Friday, the rand had depreciated against the U.S. Dollar, trading at R18.68, marking a weekly decline of -2.05%.

Chart of the Week:

The UK’s quarterly GDP growth held steady at 0% in Q3 2024, signalling a slowdown following modest gains in the first half of the year.

As always, we appreciate your support and value your trust in LNKD Investment Managers.