The U.S. election concluded with a clear victory for Donald Trump, securing Republican control of the presidency and Senate, and potentially the House as well. This “red sweep” fuelled market optimism around a pro-business agenda focused on corporate tax cuts and regulatory easing, sparking a rally that lifted the S&P 500 to its best-ever post-election gain of 2.5%. Meanwhile, the Federal Reserve announced a 0.25% rate cut this week, its first since September. Fed Chair Jerome Powell emphasised that the Fed would remain independent in its policy approach and wouldn’t respond pre-emptively to possible shifts under the new administration.

Globally, central banks moved to address evolving economic conditions. The Bank of England (BoE) reduced its interest rate by 0.25% to 4.75% for the second time this year, citing slowing inflation, with Governor Andrew Bailey signalling the possibility of further cuts. Sweden’s Riksbank also cut rates by 0.5% in response to weak economic conditions, while Norway held steady. In the eurozone, business activity showed signs of stabilising, but business confidence hit its lowest level of 2024.

In Asia, Japan’s yen strengthened following the U.S. election, with officials signalling vigilance toward excessive currency moves. China’s markets surged on new stimulus from Beijing, including a substantial RMB 10 trillion program to address local government debt and a mid-year debt ceiling increase. China also posted a robust 12.7% rise in October exports, though analysts warned that trade tensions with the U.S. could pose challenges as Trump prepares to take office in 2025.

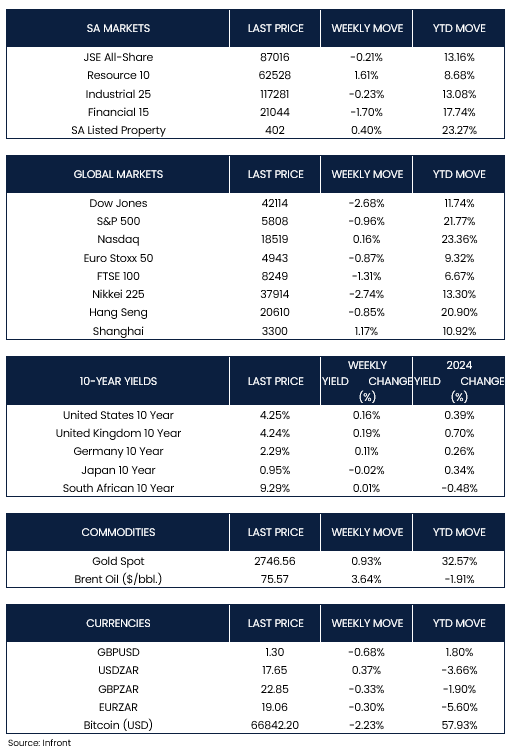

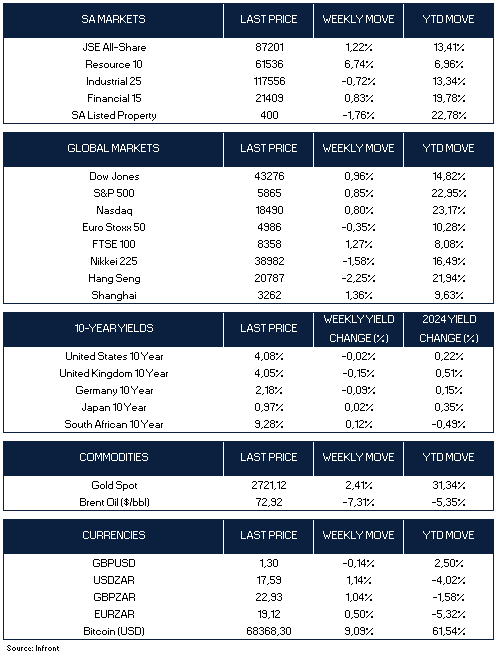

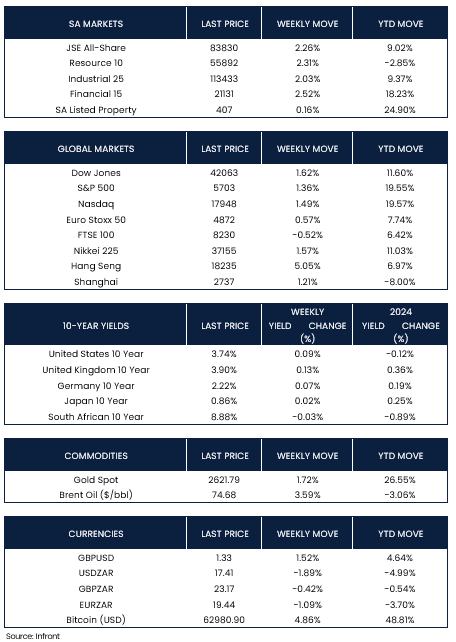

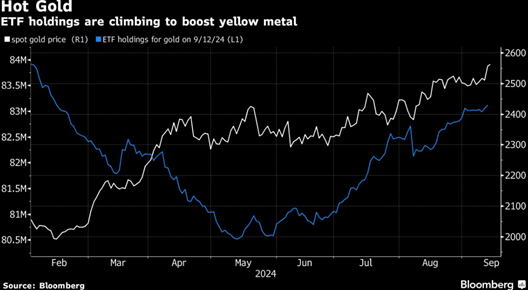

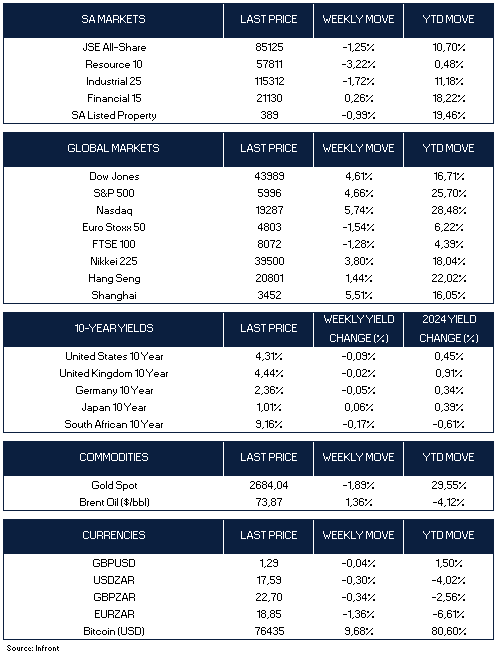

Global stock markets showed varied performance. U.S. indices recorded significant gains following Trump’s Re-election, with the Dow Jones rising by 4.61%, the S&P 500 up 4.66%, and the Nasdaq climbing 5.74%. In contrast, European markets saw downward pressure, as the Euro Stoxx 50 slipped 1.54% and the FTSE 100 declined 1.28%. Asian markets also performed well, with Japan’s Nikkei 225 advancing 3.80%, the Hang Seng gaining 1.44%, and the Shanghai Composite Index posting an impressive 5.51% increase. Meanwhile, gold prices fell 1.89% to $2,684 per ounce but remain up 29.55% for the year.

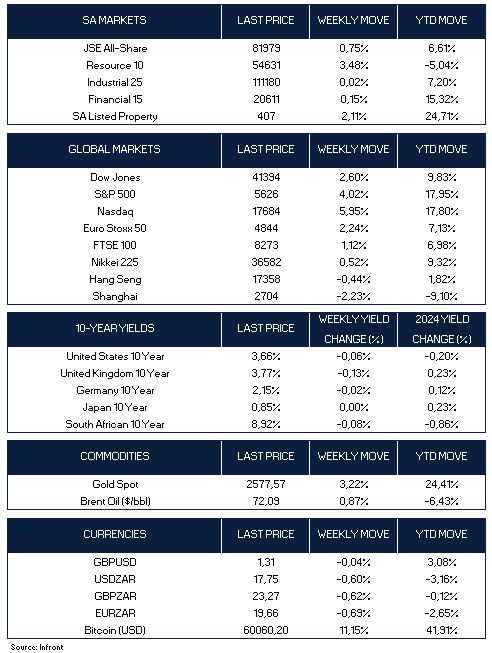

Market Moves of the Week:

In South Africa, Eskom issued a notice of intention to interrupt power supply to the City of Johannesburg and City Power over unpaid debts totalling R4.9 billion, excluding an additional R1.4 billion due at the end of November. Eskom stated that it can no longer continue absorbing the financial strain caused by the non-payment, as it forces the utility to borrow at higher premiums to cover operational costs. A final decision on power supply interruptions will be made on December 12 following consultations. Meanwhile, the closure of the Lebombo border post between South Africa and Mozambique has led to an estimated R5 billion in losses, disrupting cargo movement through the Maputo Port.

In the financial markets, South Africa saw a pullback with the JSE All Share Index declining 1.25%. The industrial (-1.72%) and resource (-3.22%) sectors saw the largest losses, while the financial sector posted a slight gain of 0.26%. The rand remained steady, closing at R17.59 to the U.S. dollar by the end of the week.

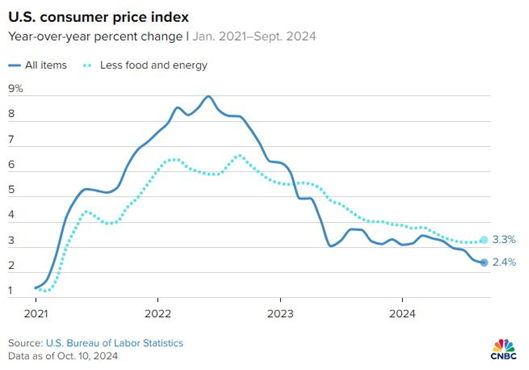

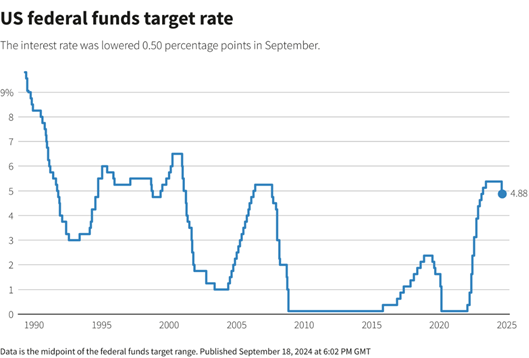

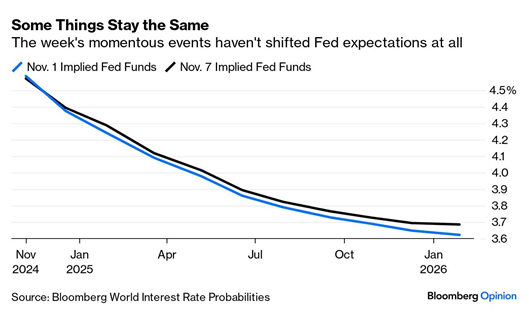

Chart of the Week:

This chart illustrates the expected path of U.S. interest rates before and after the latest FOMC meeting and U.S. election. Although the Federal Reserve cut the fed funds rate by 0.25% as anticipated, their outlook for future rate changes saw little adjustment. In his press conference, Chair Jerome Powell’s remarks left room for flexibility in future rate cuts, pending upcoming inflation reports. Meanwhile, markets responded with a continued post-election rally in equities and a reversal of recent increases in bond yields, reflecting stable investor sentiment following limited surprises from the Fed. Source: Bloomberg

As always, we appreciate your support and value your trust in LNKD Investment Managers.