The U.S. Federal Reserve held interest rates steady at 4.25% to 4.5% following its latest policy meeting, but officials signalled the possibility of two rate cuts later this year. The Fed revised its 2023 GDP growth forecast to 1.7%, from 2.1%, and raised its inflation projection to 2.7%, citing increased uncertainty driven partly by President Trump’s tariff policies, which have raised inflation expectations. Fed Chairman Jerome Powell acknowledged the high level of unpredictability in the economic landscape.

U.S. retail sales rose by 0.2% in February, recovering slightly from a revised 1.2% decline in January—the sharpest drop since November 2022, according to the Commerce Department’s Census Bureau. This modest rebound indicates subdued consumer spending, with discretionary purchases under pressure due to economic uncertainty, ongoing tariffs, and significant federal job cuts.

U.S. manufacturing production exceeded expectations in February, driven by a sharp increase in motor vehicle output. The sector, which makes up 10.3% of the economy, has shown signs of recovery, supported by the Federal Reserve’s rate cuts since September, though tariffs continue to dampen the outlook.

The Bank of England kept interest rates at 4.5% and cautioned against expectations of imminent rate cuts due to deep uncertainty surrounding the UK and global economies. The Monetary Policy Committee (MPC) voted 8-1 to maintain rates, noting growing global trade tensions, particularly those initiated by the United States. While the MPC expects inflationary pressures to ease, it made clear that monetary policy is not on a pre-set path in the coming months.

Eurozone price pressures were revised lower in February, reinforcing expectations that inflation is gradually moving toward the European Central Bank’s 2% target. Headline inflation rose 2.3% year-on-year, down from 2.5% in January, according to Eurostat data. Core inflation, excluding energy and food, eased to 2.6% from 2.7%, marking its lowest level since January 2022. Despite the easing inflation, investor expectations for future price trends remain subdued.

China’s new-home prices declined for the 21st consecutive month in February, highlighting ongoing challenges in the country’s property sector. Official data showed declines in prices, investment, and sales, suggesting that government measures and promises of additional stimulus have done little to revive demand in the crisis-hit market. New home prices edged down 0.1% month-on-month after two months of relative stability, while on a year-on-year basis, prices fell 4.8%, slightly improving from a 5.0% drop in January.

China’s economy showed modest recovery in the first two months of the year, with retail sales rising 4.0% year-on-year in January-February, an improvement from 3.7% in December and the fastest pace since November 2024. Industrial production grew 5.9%, slowing from 6.2% in December. The National Bureau of Statistics attributed the uptick to stimulus measures but also highlighted the ongoing challenges of a complex external environment, weak domestic demand, and operational difficulties for businesses.

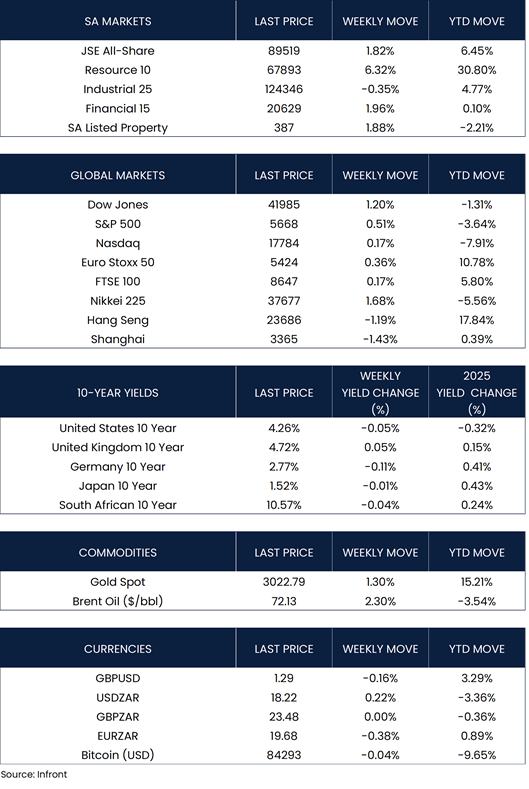

U.S. equities ended the week higher, with most major indexes reversing multi-week declines. The Dow Jones Industrial Average led gains, advancing 1.2%, while the S&P 500 added 0.51%. Large-cap technology stocks lagged, weighing on the Nasdaq Composite, which was the weakest performer.

In Europe, the Euro Stoxx 50 Index edged up 0.36% in local currency terms, while the FTSE 100 posted modest gains of 0.17%.

Asian markets were mixed. Mainland Chinese equities declined as investors turned cautious following two weeks of gains, with the Shanghai Composite Index losing 1.43%. In Hong Kong, the Hang Seng Index declined 1.19%. Meanwhile, Japan’s Nikkei 225 advanced 1.68% over the week.

Market Moves of the Week:

The South African Reserve Bank (SARB) kept its benchmark repo rate at 7.5% in its latest Monetary Policy Committee (MPC) meeting, leaving the prime lending rate at 11%. The decision to hold rates steady after three consecutive 25 basis point cuts reflects concerns over the global economic landscape. Four MPC members voted to keep rates unchanged, while two favoured a 25 basis point cut. The SARB’s decision follows the US Federal Reserve’s move to keep its benchmark rate unchanged, highlighting a more cautious global monetary policy stance.

In the holiday-shortened week, the JSE All-Share Index climbed 1.82%, with most sectors contributing to the gains. Resources led the advance, returning 6.32%, while Industrials was the sole laggard, slipping 0.35%. The rand depreciated 0.22% against the dollar, closing at R18.22/USD.

Chart of the Week:

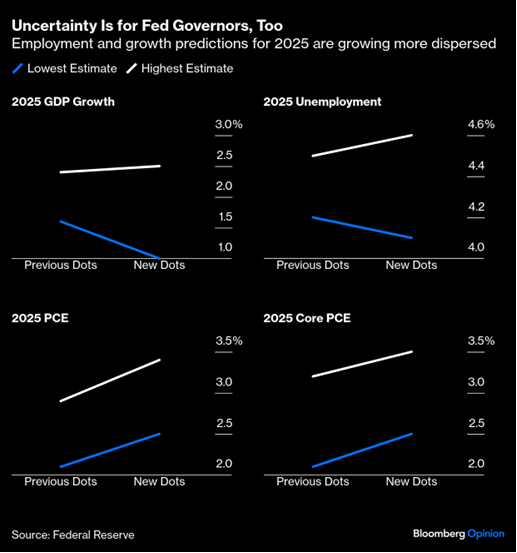

Amid growing uncertainty over the economic outlook, Fed Chairman Powell highlighted the confusion surrounding the new administration, particularly regarding tariffs. The FOMC’s latest dot-plot forecasts showed wider ranges for growth and unemployment, with inflation expectations rising. Clarity on 2025 should emerge by mid-year, but the committee’s projections remain more dispersed than in December.

As always, we appreciate your support and value your trust in LNKD Investment Managers.