The S&P 500 Index experienced its steepest weekly decline in 18 months, driven by growing concerns over an economic slowdown. The information technology sector led the downturn, with Nvidia shares particularly hard hit. Energy stocks also suffered as oil prices fell, further weighing on the index.

The week’s economic data releases largely fell short of expectations, intensifying fears that the Federal Reserve may have delayed too long in easing monetary policy. This combination of disappointing data and uncertainty around future Fed actions contributed to the broader market’s negative sentiment.

Investors closely monitored the U.S. jobs report, expecting nonfarm payrolls to rise by 165,000 and the unemployment rate to improve slightly to 4.2%. However, August’s payrolls increased by only 142,000, missing expectations and highlighting job losses in key sectors. This weaker-than-expected report may increase calls for a more aggressive monetary response, including a potential 50-basis point rate cut by the Federal Reserve later this month.

The slowdown in hiring suggests that the U.S. economy may be experiencing a soft landing—where economic growth slows but avoids a full-blown recession—so long as the deterioration in the labour market does not accelerate.

The U.S. trade deficit expanded to a two-year high in July, driven by a significant increase in goods imports. According to data released by the Commerce Department on Wednesday, the trade gap in goods and services grew by 7.9% from the previous month, reaching $78.8 billion. This figure aligned with the median forecast from a Bloomberg survey of economists.

In corporate news, Nvidia’s share price plummeted by 9.5%, erasing $278.9 billion in market value, marking the largest single-day loss in value for a U.S. stock. The decline extended to 14% over three sessions following earnings that failed to meet investor expectations. Adding to the company’s challenges, the U.S. Department of Justice issued subpoenas to Nvidia’s management as part of an investigation into potential antitrust violations.

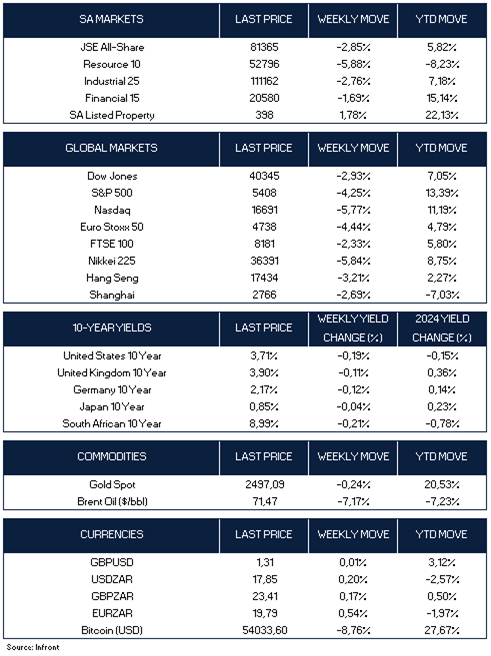

All the major US equity indexes ended the week lower, the S&P 500 -4.25%, Dow Jones -2.93%, while the tech heavy NASDAQ composite was the worst performer, closing the week down -5.77%.

The International Monetary Fund (IMF) has projected that Saudi Arabia’s current account balance is poised to shift into deficit due to declining oil prices and increasing imports tied to large-scale projects aimed at transforming the economy. The IMF’s latest Article IV review of Saudi Arabia’s economy forecasts a current account deficit of 0.1% of gross domestic product (GDP) for this year, expanding to 1.1% in 2025. The deficit is expected to average 2.9% from 2026 to 2029. This marks a stark reversal from 2022, when a surge in crude prices to nearly $130 a barrel, following Russia’s invasion of Ukraine, propelled Saudi Arabia’s current account surplus to nearly 14% of GDP.

Meanwhile, oil prices have recently hovered near a nine-month low as OPEC+ members deliberated on whether to increase supply amid ongoing concerns about global demand. This context adds pressure to Saudi Arabia’s fiscal outlook, given the nation’s heavy reliance on oil revenue.

In the Eurozone, European Central Bank (ECB) Governing Council member Gediminas Šimkus indicated in an interview that he sees a “clear case” for an interest rate cut in September. However, he expressed that the likelihood of an additional cut in October is “quite unlikely.” This statement suggests that while the ECB may continue easing monetary policy but will remain data dependent over the medium-term. The Euro Stoxx 50 closed lower, down -4.44%.

No major news out of the UK this week, however the FTSE 100 followed global peers ending the week lower, -2.33% on renewed fears about a deterioration in the outlook for the global economy.

The Japanese yen appreciated to the mid-142 range against the USD, strengthening from around JPY 145 at the end of the previous week. This movement is driven by expectations of a narrowing interest rate differential between Japan and the U.S. Market participants are increasingly anticipating that the Bank of Japan (BoJ) will raise interest rates further this year, while the U.S. Federal Reserve appears likely to cut rates in September. This shift in monetary policy outlooks has bolstered the yen against the dollar.

Japanese stocks experienced a decline over the week, with the Nikkei 225 Index down -5.84% and the broader TOPIX Index registering a 4.2% loss, yen strength posing a headwind for Japan’s export-oriented companies.

China is reportedly considering a significant interest rate cut on up to $5.3 trillion in mortgages, aiming to lower borrowing costs for millions of families while also managing the impact on the banking sector’s profitability. Financial regulators have proposed reducing rates on outstanding mortgages nationwide by approximately 80 basis points. This initiative is part of a broader package that includes speeding up the timeline for when mortgages become eligible for refinancing, according to sources familiar with the matter.

China’s official Manufacturing Purchasing Managers’ Index (PMI) fell to 49.1 in August, down from 49.4 in July, according to the National Bureau of Statistics. This decline was lower than expected and highlights deepening contractions in production and new orders, signalling ongoing challenges in the manufacturing sector as the economic slowdown continues to weigh on activity.

The Shanghai Composite index and Hong Kong’s benchmark Hang Seng Index both closed in negative territory, down -2.69% and -3.21% respectively.

Market Moves of the Week:

In South Africa, business sentiment has risen to its highest level in nearly two years, buoyed by the resumption of stable power supply, economic optimism, and political certainty following the May 29 elections. The Rand Merchant Bank and Stellenbosch University’s Bureau for Economic Research’s quarterly business confidence index increased to 38 in the three months ending September, up from 35 in the previous quarter. This improvement was primarily driven by retailers and new vehicle dealers who are anticipating a boost from expected interest rate cuts later this month.

The country’s headline GDP grew by a modest 0.4% in the second quarter of 2024, following a stagnant first quarter. The trade and finance sectors showed solid growth, rising by 1.2% and 1.3%, respectively. However, the primary sector disappointed with declines in both agriculture and mining, reflecting an economy still facing significant challenges.

On a positive note, South Africa’s current account deficit narrowed more than expected in the second quarter. The deficit reduced to an annualized 0.9% of GDP, or R64.6 billion, from a revised 1.5% in the previous quarter, driven by an increase in the rand price of exported goods and services.

Additionally, September 1st marked the beginning of a new era for the retirement savings industry with the introduction of the Two Pot system. This reform allows retirement fund members to access a portion of their assets before retirement age, providing liquidity for emergency funding needs, particularly in the wake of the pandemic. While similar reforms have been implemented in other countries, the impact on South Africa’s collective investment market and economic stimulus will be closely monitored by all market participants.

The JSE ALSI also ended the week lower tracking the risk off sentiment from global peers, down -2.85%. All the major sectors were lower this week, led by Resources down -5.88%, followed by Industrials down -2.76%, while Financials fared best, but still closed in negative territory down -1.69%. The SA Listed Property sector was the outlier this week closing in the green, up 1.78%. The Rand closed slightly weaker against the Dollar, ending the week at R17.85/$.

Chart of the Week:

Analysts are increasingly doubtful that China will achieve its 5% economic growth target for 2024. The median forecast for full-year GDP growth among economists surveyed by Bloomberg has declined to 4.8%, down from 4.9% in mid-August. This shift in sentiment follows weaker-than-expected second-quarter growth of 4.7% reported in July, which prompted several leading financial institutions to lower their growth projections. Goldman Sachs, Citi, and Barclays all adjusted their forecasts in July, reducing their targets from 5% to 4.9%, 4.8%, and 4.8% respectively. JPMorgan is even more cautious, anticipating growth of just 4.6% for the year. Source: Bloomberg and Financial Times.

As always, we appreciate your support and value your trust in LNKD Investment Managers.