In the U.S., lower oil prices helped set a more positive tone for markets. Brent crude fell sharply as hopes of a U.S.–Iran agreement raised expectations that energy flows through the Strait of Hormuz could improve. The move helped ease near-term inflation concerns and supported risk appetite across equity and bond markets.

Inflation remained the key macro focus. The April PCE price index rose 0.4% month-on-month and 3.8% year-on-year, while core PCE increased 3.3% year-on-year. The Federal Reserve also maintained a cautious tone, with several policymakers still focused on the risk that the recent energy shock and supply disruptions could keep inflation elevated.

Growth data was more mixed. First-quarter GDP was revised down to 1.6% from an initial estimate of 2.0%, reflecting softer investment and consumer spending. Durable goods orders rose 7.9% in April, driven mainly by transportation equipment, but the underlying detail was weaker, with core capital goods orders, a proxy for business investment, falling 1.1% after a strong March gain.

The consumer picture was also uneven, as personal spending rose 0.5%, while personal income was broadly flat.

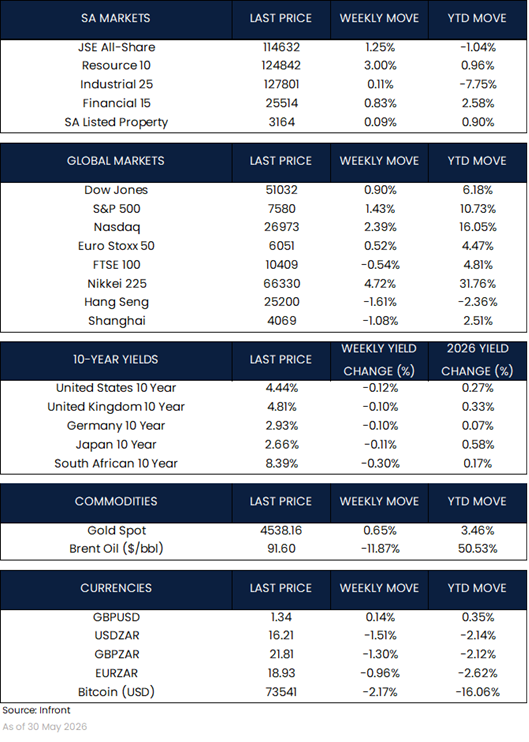

Despite the mixed data, U.S. equities ended higher. The S&P 500 rose 1.43%, while the Nasdaq gained 2.39%. Treasury yields moved lower, with the 10-year yield ending at 4.44%, as lower oil prices and reported progress in U.S.–Iran negotiations helped ease inflation concerns.

In Europe, the week was steadier, but not especially strong. The Euro Stoxx 50 gained 0.52%, with Germany’s DAX and France’s CAC 40 also ending higher, while the FTSE 100 declined 0.54%. Lower oil prices helped improve the tone, particularly given Europe’s exposure to energy costs, but the region still faced a difficult mix of soft growth and uncertain inflation dynamics.

The European Central Bank’s April minutes showed that some policymakers were still open to raising rates, with officials concerned that the recent energy shock could prove more persistent than initially expected. Germany’s labour market data was slightly more encouraging, with unemployment unexpectedly easing to 6.3%, although the outlook remains cautious.

In the UK, shop price inflation rose more than expected to 1.2% year-on-year in May, reflecting higher shipping and raw material costs linked to the Middle East conflict. Food inflation eased, but the data still pointed to pressure on household spending.

In Asia, Japan was the clear outperformer. The Nikkei 225 rose 4.72%, supported by lower oil prices and renewed demand for technology and semiconductor shares. Softer inflation data also reduced some near-term pressure on the Bank of Japan to raise rates quickly, although officials continued to signal that policy may still need to adjust over time.

China’s industrial profit data was more encouraging, with profits rising 24.7% year-on-year in April and pointing to improved conditions in parts of the industrial economy. However, markets remained cautious, as investors continued to look for clearer evidence that policy support is feeding through into broader demand.

Chinese policymakers are expected to introduce new financing tools to support infrastructure investment. At the same time, concerns around coal supply resurfaced after a mine accident in Shanxi pushed coking coal prices higher. Despite stronger industrial profit data, Chinese equities ended weaker, with the Shanghai Composite and Hang Seng both declining over the week.

Market Moves of the Week:

In South Africa, the SARB raised rates by 25 basis points to 7.00%, its first hike in three years. The decision was driven by concern that the recent energy shock and global supply risks could keep inflation elevated. Producer inflation also surprised to the upside, rising 4.8% year-on-year in April, reinforcing the central bank’s cautious stance.

Moody’s revised South Africa’s outlook to positive, citing an improving fiscal position and continued reform efforts. Transnet bulk export data was also encouraging, with April bulk exports remaining firm year-on-year and year-to-date performance supported by stronger flows through Saldanha and Richards Bay. These developments remain important for mining exports, tax revenue and broader confidence in the reform story.

Local markets ended higher, supported by the improved global backdrop and stronger resource shares. The JSE All Share Index rose 1.25%, while the Resource 10 Index gained 3.00%. South African bonds also strengthened, with the 10-year yield ending at 8.39%. The rand firmed to R16.21 against the U.S. dollar, helped by lower oil prices, a softer dollar and improved sentiment toward emerging markets.

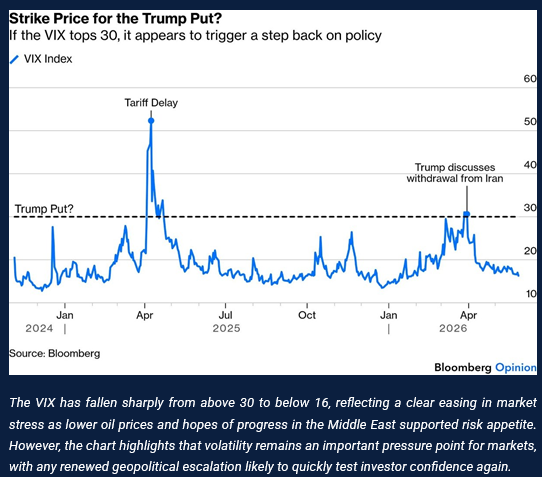

Overall, the week was defined by a clear easing in market stress. Hopes of progress in the Middle East, lower oil prices and continued AI momentum supported equities, while volatility eased sharply, with the VIX moving from above 30 to below 16. However, the broader macro picture remains less settled: U.S. inflation is still persistent, consumer momentum remains mixed, China’s recovery is uneven, and South Africa has shifted back into tightening mode.

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Manager..