If investors needed a reminder that geopolitics and artificial intelligence remain two of the year’s dominant market drivers, the start of the third quarter provided one. Renewed hostilities between the United States and Iran pushed oil prices higher and briefly unsettled markets, but the equity market reaction was contained. Investors largely treated the escalation as a source of near-term headline risk, while renewed strength in semiconductor and AI shares helped the S&P 500 and Nasdaq recover from earlier weakness.

In the United States, minutes from the Federal Reserve’s June meeting showed that policymakers remain divided over the path for interest rates. A few officials saw a case for raising rates, although they ultimately supported leaving borrowing costs unchanged. Most also favoured removing language that implied an easing bias, reflecting uncertainty around persistent inflation, AI related demand and geopolitical risks.

Economic data remained broadly resilient. The ISM services index eased slightly to 54.0 in June but remained in expansion territory for a 24th consecutive month, while its employment component returned to growth. Initial jobless claims declined to 215,000 and continuing claims rose only modestly, suggesting that the labour market is cooling gradually rather than weakening sharply. Housing remained softer, with existing home sales falling by 2.4% as high prices and borrowing costs continued to constrain affordability.

In Europe, the renewed conflict between the United States and Iran raised concerns that higher energy prices could keep inflation and interest rates elevated. Germany offered some relief as annual inflation slowed to 2.3% in June from 2.6% in May. Other data were generally encouraging, with Dutch household consumption growing at its fastest pace in more than a year, German exports rising unexpectedly and Sweden recording a third consecutive month of economic growth while inflation eased slightly.

In the United Kingdom, politics took centre stage after Andy Burnham secured the support of 322 of Labour’s 403 Members of Parliament in the contest to replace Keir Starmer. Investors will be watching for clarity on his economic priorities, fiscal approach and cabinet appointments. The housing market remained subdued, with both new buyer enquiries and agreed sales still firmly negative as elevated mortgage costs continued to weigh on demand.

In Japan, the ten-year government bond yield ended the week near 2.78%, despite briefly reaching its highest level since 1996. Yields later eased after Finance Minister Satsuki Katayama called on pension funds to increase allocations to domestic assets. Economic data continued to show persistent inflationary pressures, with wholesale prices rising by 7.1% year on year in June. Nominal wages increased by 3.2% in May, but real wage growth slowed to 1.4%, while household spending declined by a smaller than expected 0.4%, suggesting that consumer demand remained relatively resilient.

In China, AI and semiconductor developments supported technology shares early in the week, although some gains were later reversed as investors took profits. Inflation data highlighted the divide between weak consumer demand and rising producer costs, with consumer inflation slowing to 1.0% in June while producer prices rose by 4.1%, the fastest pace in nearly four years. The People’s Bank of China maintained its supportive policy stance and pledged further assistance for domestic demand, technology investment and smaller businesses, but stopped short of announcing broad stimulus.

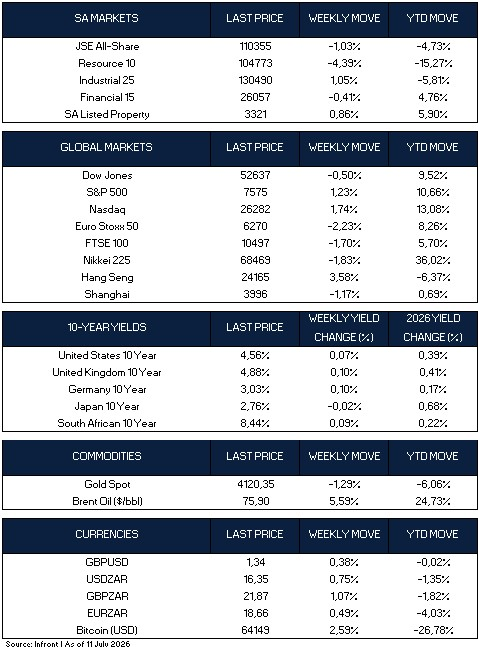

Overall, global markets ended the week on a mixed note. United States equities were broadly positive, with the S&P 500 gaining 1.23% and the Nasdaq rising by 1.74%, while the Dow Jones declined by 0.50%. European markets came under pressure, with the Euro Stoxx 50 and FTSE 100 falling by 2.23% and 1.70% respectively. Asian markets were mixed, as the Hang Seng gained 3.58%, while the Nikkei 225 and Shanghai Composite declined. Government bond yields rose across the United States, United Kingdom and Germany, while Japanese yields edged lower. In commodities, gold fell by 1.29%, while Brent crude oil rose by 5.59% and remains sharply higher year to date. Bitcoin gained 2.59% for the week but remains down by 26.78% in 2026.

Market Moves of the Week:

The outlook for South African interest rates became slightly more supportive after South African Reserve Bank Governor Lesetja Kganyago suggested that the inflationary impact of the Iran conflict may prove temporary, particularly if oil prices remain contained. This marked a softer tone than his comments a week earlier, when he focused more heavily on rising inflation expectations. The July Monetary Policy Committee meeting is therefore now more likely to leave interest rates unchanged rather than increase them by 0.25%, although the decision remains finely balanced.

The inflation outlook has also improved modestly, supported by lower oil prices and a firmer rand. Forecasts point to average inflation of around 3.9% in 2026 and 3.0% in 2027, with inflation potentially falling below 4% in the final quarter of this year. Should these trends continue, the Reserve Bank may be able to resume interest rate cuts in the first quarter of 2027, offering gradual support to household finances, bonds, listed property and other interest rate sensitive assets.

The broader economy remains under pressure. Manufacturing production fell by 4.3% in the year to May, after declining by 2.9% in April, although monthly output improved by 1.1%. Producers continue to face high operating, infrastructure and fuel costs, as well as pressure from United States tariffs. South Africa’s net foreign exchange reserves also declined to $71.34 billion in June from $73.47 billion in May. The improving inflation outlook is encouraging, but weak industrial activity reinforces the need for faster reform and better infrastructure.

Against this backdrop, South African markets ended the week weaker. The JSE All Share Index declined by 1.03%, with the sharpest pressure coming from resource shares, which fell by 4.39% and are now down by 15.27% year to date. Financials declined by 0.41%, while industrials and listed property were the relative bright spots, gaining 1.05% and 0.86% respectively. The rand weakened against major currencies, with the United States dollar ending the week at R16.35, while the South African ten-year government bond yield rose to 8.44%.

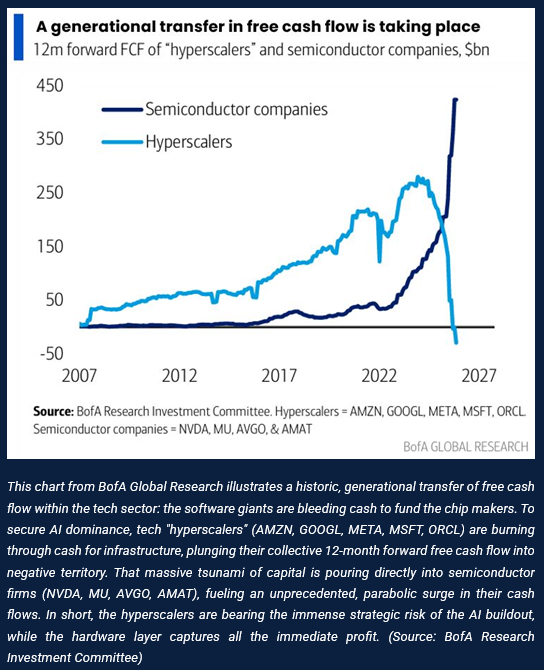

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.