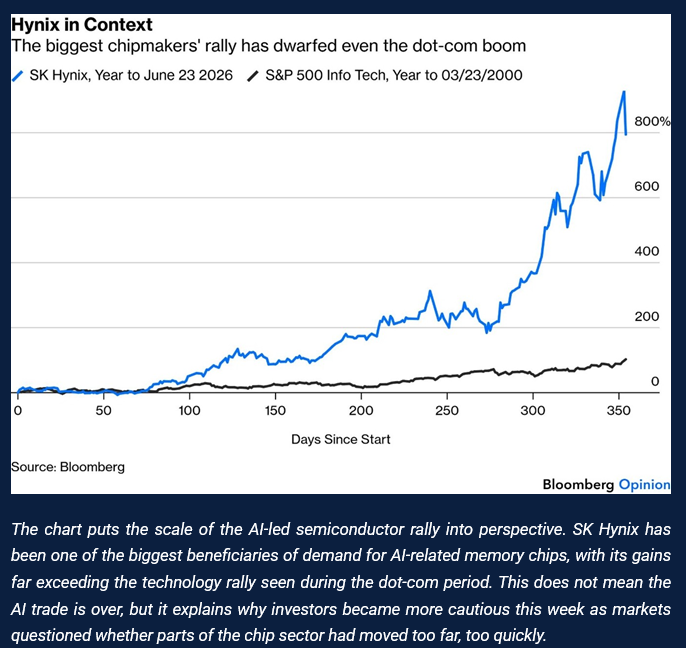

Global markets were volatile over the week as attention shifted from oil relief to renewed pressure in technology and AI-linked shares. The sell-off began in U.S. megacap technology before spreading into semiconductors, with Korea’s KOSPI falling sharply and the SOX chip index declining around 8% as investors questioned how far the AI trade had already run.

Micron Technology’s strong earnings update briefly steadied sentiment, but the rebound faded quickly. That left investors debating whether the pullback was normal quarter-end volatility or a sign that positioning in AI-linked shares had become stretched.

Monetary policy uncertainty added to the pressure. U.S. PCE inflation rose to 4.1% year-on-year in May, while core PCE increased to 3.4%, keeping attention on whether the Federal Reserve may need to keep policy restrictive for longer.

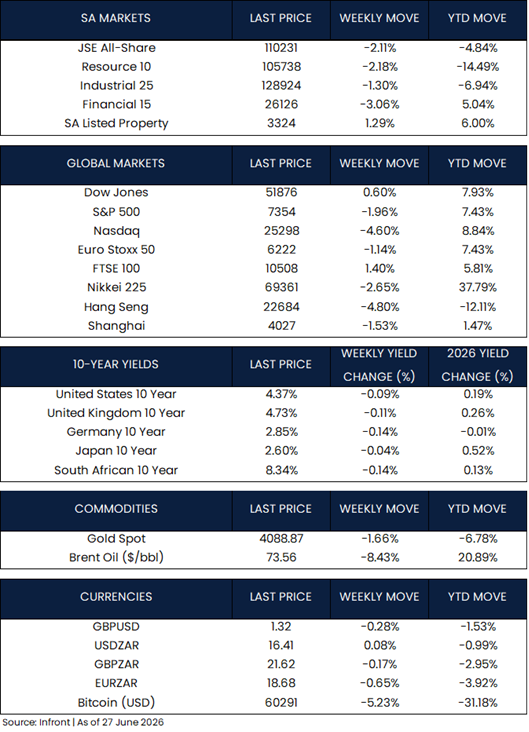

U.S. equities were mixed over the week. The Nasdaq fell 4.60% and the S&P 500 declined 1.96%, weighed down by renewed pressure in large-cap technology and AI-linked shares. The Dow Jones, however, gained 0.60%, showing that the sell-off was concentrated in large-cap growth and technology shares. On the data front, first-quarter U.S. GDP was revised higher to an annualised 2.1% from 1.6%, helped by lower imports, while consumer spending was revised down. Business activity also improved in June, with the composite PMI rising to 52.2, its highest level in five months, while manufacturing activity reached its strongest level since May 2022.

In Europe, inflation expectations eased, with the ECB’s latest consumer survey showing that 12-month inflation expectations declined to 3.5% in May, the lowest level in three months. With oil prices also moving back toward pre-conflict levels, this helped ease some of the inflation pressure facing the ECB. In the UK, Prime Minister Keir Starmer announced his resignation on 22 June 2026. Domestic data was weaker, with retail sales volumes falling sharply in June and the CBI balance declining to -54 from -46 in May, while manufacturing order books fell to -45, their weakest level since 2020.

In Japan, inflation and Bank of Japan policy remained in focus. Tokyo core CPI rose to 1.6% year-on-year in June from 1.3% in May, the first pickup in eight months, keeping investors focused on whether the BoJ may need to tighten policy further.

Japanese equities weakened over the week, with the Nikkei 225 falling 2.65%. Local AI and semiconductor-linked names remained sensitive to the broader global technology sell-off, which weighed on the index into the end of the week.

In China, investor sentiment remained weak, with technology shares under pressure. Investors had favoured other Asian technology markets earlier in the week, but the broader semiconductor sell-off later weighed on the sector. The softer tone was reinforced by weaker recent activity data, with Goldman Sachs lowering its second-quarter GDP forecast to 3.5% quarter-on-quarter annualised from 4.0%, although it kept its full-year growth forecast unchanged at 4.7%.

Market Moves of the Week:

In South Africa, producer inflation was the main local data point, accelerating to 7.8% year-on-year in May from 4.8% in April. The increase pointed to renewed pipeline cost pressure in the economy, reinforcing the risk that higher input costs could still feed through into consumer inflation.

The growth backdrop also remained under pressure, with S&P lowering its South African growth forecasts for 2026 and 2027 to 1.3% and 1.5%, respectively, while raising its 2026 inflation forecast to 4.3%. This points to a less comfortable mix of softer growth and higher inflation.

South African markets ended the week weaker, with the JSE All Share Index lower. Financials were the weakest major sector, falling 3.06%, while Resources declined 2.18% and Industrials lost 1.30%. Listed property was the standout performer, rising 1.29%. The rand was broadly stable against the U.S. dollar at R16.41, while the South African 10-year government bond yield moved lower to 8.34%.

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.