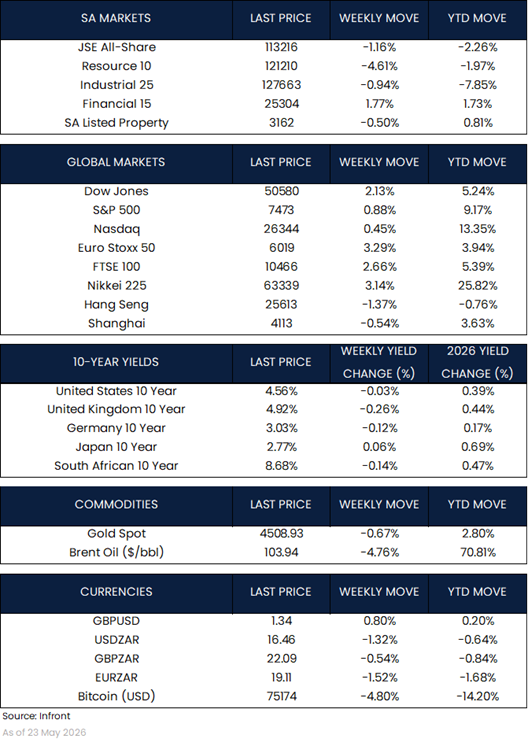

Major global equity markets were mostly stronger over the week, supported by renewed momentum in artificial intelligence-related shares and hopes that tensions in the Middle East could ease. In the U.S., the Dow Jones gained 2.13%, while the S&P 500 rose 0.88% to record its eighth consecutive weekly gain. The Nasdaq advanced 0.45%, while small-cap shares outperformed, with the Russell 2000 rising 2.72%.

There was also a clear shift in market leadership. Investors continued to favour Japan, Korea and AI/semiconductor-linked areas, while China and Hong Kong technology shares lagged. Sector preference also leaned toward areas better positioned for higher oil and inflation, including coal, oil, food retailers and drug retailers, while discretionary retail, travel and leisure, and real estate remained more vulnerable.

U.S. economic data was more mixed. The S&P Global flash composite PMI held steady at 51.7 in May, with stronger manufacturing activity offset by slower growth in the services sector. The manufacturing PMI rose to 55.3, its strongest level in four years, while the services index declined to 50.9.

However, price pressures remained a key concern, with input costs rising to their highest level since late 2022 and selling price inflation reaching its highest level since August 2022. Consumer sentiment was weaker. The University of Michigan consumer sentiment index fell to a record low of 44.8, while year-ahead inflation expectations increased to 4.8%.

U.S. monetary policy also remained in focus after Kevin Warsh was sworn in as the new Federal Reserve Chair. Since his nomination, higher oil prices and inflation concerns have pushed markets to price a higher path for interest rates, with futures now implying that the Fed funds rate could remain above 4% by July 2027. The U.S. 10-year Treasury yield also moved up to a midweek high of 4.69%, as investors adjusted to the risk that rates may stay higher for longer.

European equities also strengthened as global sentiment improved and investors took comfort from hopes of de-escalation in the Middle East. The Euro Stoxx 50 gained 3.29%, while the UK’s FTSE 100 advanced 2.66%. The macro backdrop was less supportive, with the European Commission lowering its 2026 eurozone growth forecast to 0.9% and raising its inflation forecast to 3.0%. German PPI also rose to 1.7% in April, driven mainly by intermediate goods and mineral oil prices.

In the UK, labour market data weakened, with unemployment rising to 5.0% in the three months to March and job openings falling to their lowest level in five years. Inflation, however, provided some relief, slowing to 2.8% in April from 3.3% in March and coming in below expectations.

In Asia, Japan led gains as technology and semiconductor shares benefited from the broader AI theme. The Nikkei 225 gained 3.14%, while the broader TOPIX rose 0.74%. Japan’s first-quarter GDP also came in ahead of expectations, expanding at an annualised rate of 2.1%, up from 0.8% in the prior quarter.

Inflation data in Japan was softer than expected. Core CPI slowed to 1.4% year-on-year in April, remaining below the Bank of Japan’s 2% target for a third consecutive month. This reduced near-term pressure on the Bank of Japan to tighten policy, although Japanese government bond yields remained elevated.

Chinese equities ended lower after April activity data suggested that the recovery was losing momentum. The Shanghai Composite fell 0.54%, while the Hang Seng lost 1.37%.Industrial production rose 4.1% year-on-year, slowing from 5.7% in March, while retail sales increased only 0.2%, the weakest growth since late 2022. Fixed asset investment also contracted 1.6% over the January to April period.

The People’s Bank of China left benchmark lending rates unchanged for a 12th consecutive month, with the one-year loan prime rate at 3.00% and the five-year rate at 3.50%. For China, the key issue remains whether targeted policy support will be enough to stabilise domestic demand, particularly as consumer activity and investment momentum remain weak.

Market Moves of the Week:

In South Africa, inflation and the upcoming SARB decision remained the major local focus. April CPI accelerated to 4.0% year-on-year from 3.0% in March, driven mainly by higher fuel prices. This kept attention on whether the latest oil shock could feed into broader inflation pressures. FRA markets were pricing in roughly 25bps of additional tightening, while Standard Bank expects the SARB to hike by 25bps at the upcoming MPC meeting.

The main concern is that higher oil prices could make inflation harder to control, especially if food prices also rise later in the year. Growth also remains under pressure, with weaker manufacturing partly offset by better mining production. Improving port and rail performance remains one of the more positive medium-term developments.

South African government bonds also remained in focus ahead of the SARB decision. Although near-term inflation risks have increased, relatively attractive yields and support from still-elevated commodity prices continue to provide some medium-term support for local bonds.

South African equities ended the week lower as investors remained focused on oil prices, global sentiment and the upcoming SARB decision. The JSE All-Share declined 1.16%, with the Resource 10 falling 4.61% and the Industrial 25 down 0.94%. Year-to-date, the All-Share is down 2.26%.

Chart of the Week:

As always, we appreciate your support and value your trust in STRATEGIQ Capital.