Global markets experienced a more volatile week as investors digested a mix of economic data, earnings releases and ongoing geopolitical and trade uncertainty. While headlines around artificial intelligence and credit markets unsettled sentiment, underlying economic indicators continue to point to a global economy that is slowing in parts but remains broadly resilient.

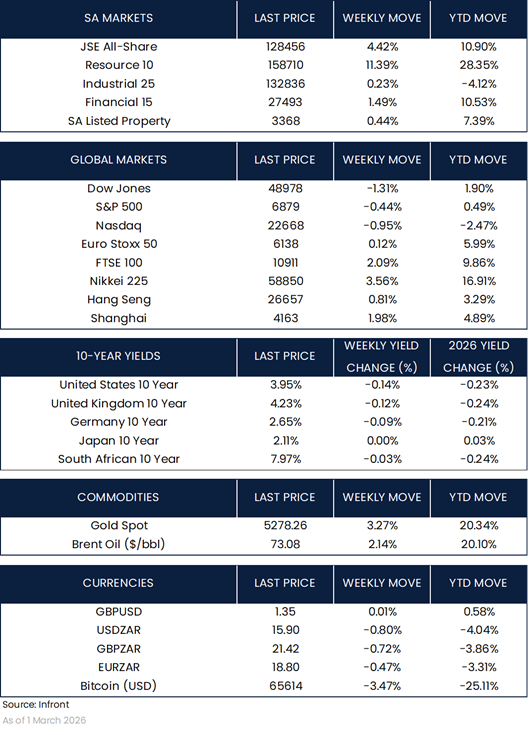

In the United States, equity markets ended the week lower. The Dow Jones declined 1.31%, the S&P 500 fell 0.44% and the Nasdaq lost 0.95%. Early in the week, markets sold off after a widely circulated research paper reignited concerns about the potential disruptive impact of artificial intelligence across various industries. The report amplified existing nervousness around whether AI could accelerate structural shifts in business models and earnings patterns. Sentiment stabilized midweek ahead of NVIDIA’s quarterly results. Although the company delivered earnings that beat expectations, the strong numbers were not enough to fully reverse the cautious tone, and markets drifted lower into the weekend.

On the economic front, producer price inflation surprised slightly to the upside, rising 0.5% month on month in January and 2.9% year on year, driven largely by services prices. Factory orders declined in December, reflecting some softness in parts of the manufacturing sector. Consumer confidence improved modestly to 91.2, suggesting households remain cautious but not overly pessimistic. Initial jobless claims edged up to 212,000 but continue to point to a labour market that remains relatively stable. U.S. government bond yields moved lower during the week, with the 10-year Treasury yield declining to 3.95%, as investors sought some safety amid equity market volatility.

In the United Kingdom and Europe, markets were more resilient. The Euro Stoxx 50 rose 0.12% for the week and is now up 5.99% year to date, while the FTSE 100 gained 2.09%, taking its year to date performance to 9.86%. European equities have continued to benefit from solid corporate earnings and investor interest in diversifying beyond the U.S. technology-heavy market. German business confidence improved again in February, while inflation readings across the region were mixed but generally consistent with gradual easing price pressures. In the UK, consumer confidence slipped slightly, reflecting ongoing cost pressures, although comments from Bank of England officials about potential interest rate cuts in 2026 provided some support. Bond yields in both the UK and Germany eased modestly over the week.

Asian markets delivered stronger performance. In Japan, the Nikkei 225 rallied 3.56%, extending its year to date gain to 16.91%. Investors remain constructive on Japan’s policy direction and corporate reform momentum. Inflation data in Tokyo came in slightly ahead of expectations, reinforcing the view that the Bank of Japan will likely continue with a gradual and measured approach to adjusting interest rates.

In China, markets also advanced, with the Shanghai Composite rising 1.98% and the Hang Seng gaining 0.81%. Trading volumes improved following the Lunar New Year break, and attention is turning to upcoming policy meetings where economic targets and stimulus measures are typically outlined. The People’s Bank of China adjusted certain foreign exchange policy settings in what is seen as a move to manage currency volatility rather than signal a major change in direction.

Market Moves of the Week:

South African markets were among the strongest performers this week. The JSE All Share Index rose 4.42%, bringing its year to date gain to 10.90%. The Resources sector led the advance with an 11.39% weekly gain and is now up 28.35% year to date, supported by firm commodity prices. Financials gained 1.49%, while Industrials edged up 0.23% but remain negative for the year. Listed property rose 0.44%. Gold increased 3.27% and Brent crude oil gained 2.14%, providing additional support to the local bourse. The rand strengthened to 15.90 against the U.S. dollar, while the South African 10-year government bond yield declined to 7.97%.

The national budget was broadly well received by markets. Government maintained its projection that debt will peak this fiscal year at 78.9% of GDP before gradually declining over the medium term. Although near term deficit projections were slightly wider, the overall debt path remains stable. A reduction in weekly government bond issuance supported the local bond market. Several tax changes were announced, including an increase in the annual Tax Free Savings Account contribution limit to R46,000, a higher annual capital gains tax exclusion of R50,000 and an increase in the primary residence capital gains exclusion to R3 million. The single discretionary allowance was increased to R2 million per calendar year, and further clarity was provided on the regulatory treatment of crypto assets.

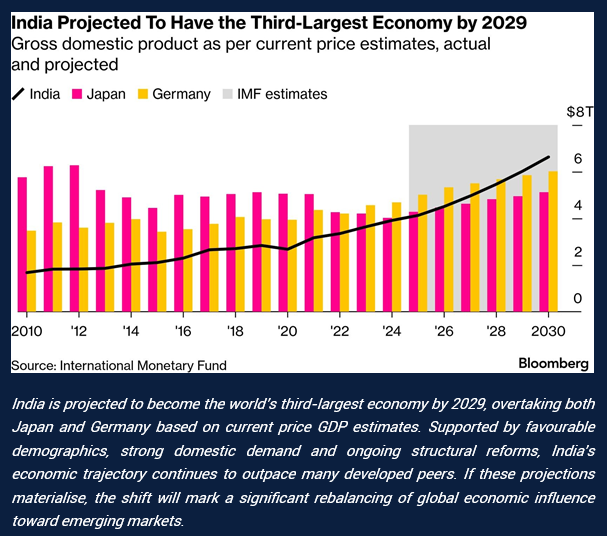

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.