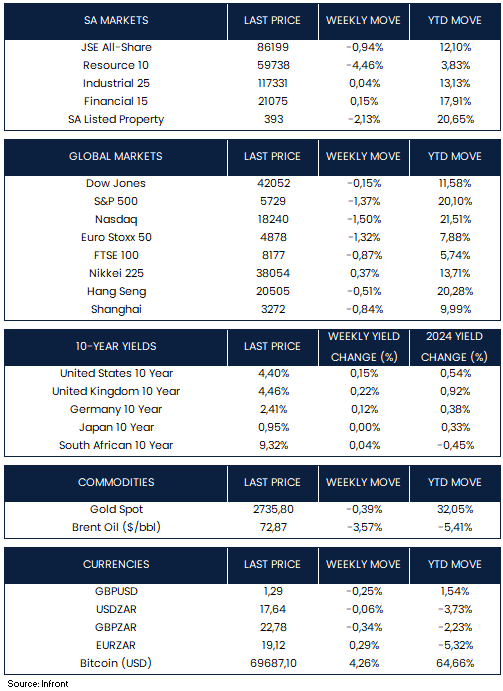

Major U.S. indexes closed mostly lower after a particularly eventful week for economic and earnings announcements. Growth stocks generally underperformed value shares, partly due to cautious earnings reports from Meta Platforms and Microsoft. Small-cap stocks also fared notably better than large-caps. The S&P 500 fell 1.37% w/w, while the Dow Jones Industrial Average dipped -0.15%. The tech-heavy Nasdaq Composite dropped by -1.50% over the week. The yield on the U.S. 10-year Treasury note rose by 0.11% from a week ago to 4.30% despite soft U.S. payrolls.

U.S. nonfarm payrolls increased by only 12,000 in October, well below expectations. The numbers were likely skewed by hurricane impacts and a Boeing machinist strike, which cut 44,000 jobs. Despite the noise in these figures, other indicators, like weekly jobless claims, don’t suggest broad weakness. Markets have priced in a 0.25% rate cut by the Federal Reserve next week, with another likely in December.

The Institute for Supply Management (ISM) reported that its manufacturing index fell for the seventh consecutive month in the U.S., reaching 46.5, a 15-month low. The ISM chair noted that demand remains weak as companies hesitate on capital and inventory investments, citing concerns over inflation and uncertainties in federal monetary policy amid proposed fiscal policies from both major parties.

The PCE price index, a key inflation measure for the Fed, rose 0.1% in August, bringing the annual inflation rate to 2.2%. This was below Wall Street expectations and marked the lowest level since early 2021.

The eurozone economy grew 0.4% in the third quarter, twice the pace of the previous quarter and above the 0.2% consensus forecast. Germany unexpectedly avoided a recession with growth of 0.2%. Annual headline inflation rose to 2% in October, up from 1.7% in September, slightly surpassing expectations. The Euro Stoxx 50 fell 1.32% over the week.

The yield on two-year UK gilts increased by over 0.25% following Chancellor Rachel Reeves’s announcement of the Labour Party’s inaugural budget. The plan will increase taxes by £40 billion annually by 2030 and spending by £74 billion. A revised debt definition will enable the government to borrow an additional £100 billion, primarily for infrastructure projects. Additionally, the employer’s National Insurance tax will increase, raising concerns among economists about potential negative impacts on employment and wage growth. Moody’s and S&P expressed scepticism regarding the new debt definition. The FTSE 100 dipped by -0.87% w/w.

The Standing Committee of China’s National People’s Congress will meet next week to discuss boosting domestic demand and meeting GDP growth targets, as stated by Vice Finance Minister Liao Min. Analysts expect the upcoming stimulus to stabilize growth, with over ¥10 trillion ($1.4 trillion) in new bonds projected. Notably, the manufacturing PMI rose to 50.1 in October, marking its first expansion since April, and residential property sales also increased year-on-year for the first time in 2024.

Chinese stocks retreated despite data showing a pickup in economic activity. The Shanghai Composite Index fell -0.84% w/w. Elsewhere in Asia, Japan’s stock markets rose over the week, with the Nikkei 225 Index gaining 0.37%, as the Bank of Japan (BoJ) held rates steady amid political uncertainty.

Market Moves of the Week:

In South Africa, The Midterm Budget Policy Statement (MTBPS) was delivered on Wednesday, revealing that South Africa’s finances are facing challenges. Key points included:

- Growth Forecasts: Treasury has slightly lowered South Africa’s GDP growth forecast to 1.1% for 2024 due to weak early-year activity, with small adjustments for the following years. Growth is expected to average around 1.8% from 2025 to 2028, helped by global stability and domestic reforms.

- Revenue Shortfall: This year’s tax revenue is expected to be R22 billion lower than projected, mostly because of a weak job market and reduced demand for imports.

- Higher Spending: Government spending will increase by 6% this year, above earlier projections, due to more spending on infrastructure, wages, and debt. Future spending will be moderated but still high due to social welfare needs.

- Budget Deficit and Debt: The budget deficit will widen to 5% of GDP. Debt will peak at 75.5% of GDP and decline slowly over the next decade. Finance Minister Enoch Godongwana emphasized the need for fiscal discipline to manage debt and ensure long-term fiscal stability.

- Policy Moves: A fiscal rule to manage spending changes is being developed, with recommendations expected in early 2025. A review of the inflation-targeting framework is also underway.

In other news, The Absa Purchasing Managers’ Index (PMI) dipped to 52.6 points in October from 53.3 in September, marking the second month above 50 (>50 indicates an expansion). The business activity index, which provides a more focused view of how much activity is taking place in the manufacturing or services sector, rose significantly by 4.1 points to 55.6, indicating improved production and a recovery in the manufacturing sector.

The All-Share Index dipped by 0.94% this week, dragged down by Resources (-4.46%). The local currency marginally strengthened against the U.S. dollar, dropping to R17.64/$ from last week’s R17.65/$ level. SA government bonds remained relatively stable, as yields on the 10-year rose 0.04% over the week.

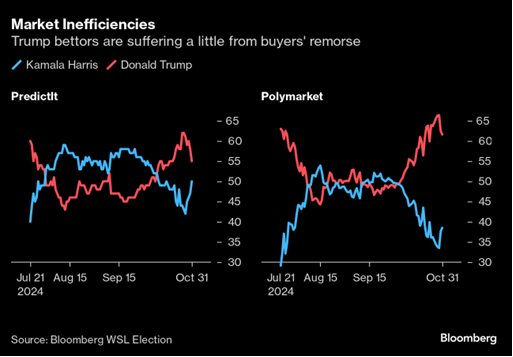

Chart of the Week:

Market Sentiment Shifts: Confidence in Trump’s Chances Wavers as Betting Markets Adjust Odds – Polymarket remains more bullish than PredictIt, but both have pared down his prospects this week. Buyers’ remorse suggests traders may have overplayed their hand. Source: Bloomberg.

As always, we appreciate your support and value your trust in LNKD Investment Managers.