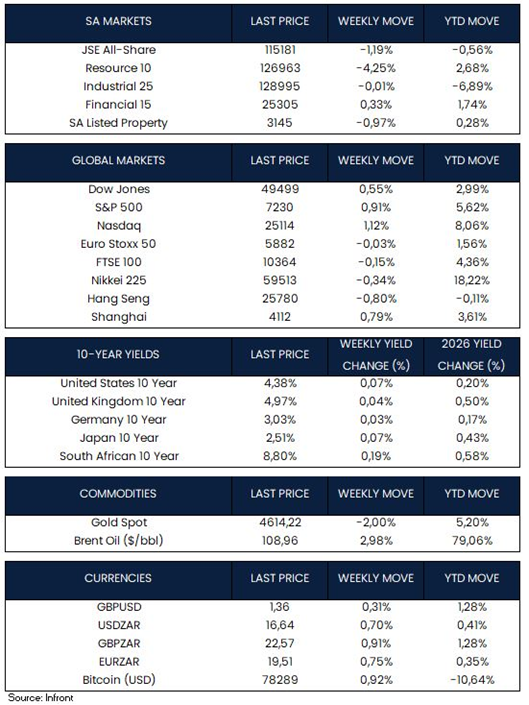

US equities delivered solid gains this week, driven by another strong US earnings season. For the week the S&P 500 rose 0.9% while the tech-heavy Nasdaq gained 1.1%, both closing at record highs. April was the standout month with the S&P 500 returning over 10%, its best performance since November 2020.

With more than half of S&P 500 companies having reported, results are coming in robustly. Five of the Magnificent Seven beat or met expectations. Apple surged on strong iPhone demand and resilient China sales. Alphabet jumped on accelerating AI and cloud revenue. Meta fell sharply after announcing another increase in AI capex. ExxonMobil and Chevron beat profit expectations, though their shares were muted as Iran submitted a new peace proposal to mediators, raising hopes for an eventual resumption of Persian Gulf oil exports.

On the data front, US Manufacturing PMI held at 52.7 in April, matching a near four-year high but missing consensus. New orders accelerated, while employment fell at its sharpest pace in four months and input prices surged at the fastest rate since late 2021.

The Federal Open Market Committee (FOMC) held rates steady at 3.50%–3.75%, but the meeting carried more noise than usual. Three voting members dissented against retaining the “easing bias” language, while a fourth voted to cut, the largest number of dissents under Powell. The statement upgraded inflation from “somewhat elevated” to simply “elevated,” adding that this only partly reflects higher energy prices, signalling the Fed sees broader inflationary forces at work. Powell confirmed he will remain on the Board of Governors beyond his tenure as chair, citing ongoing legal proceedings against the Fed. Kevin Warsh has been named as incoming chair.

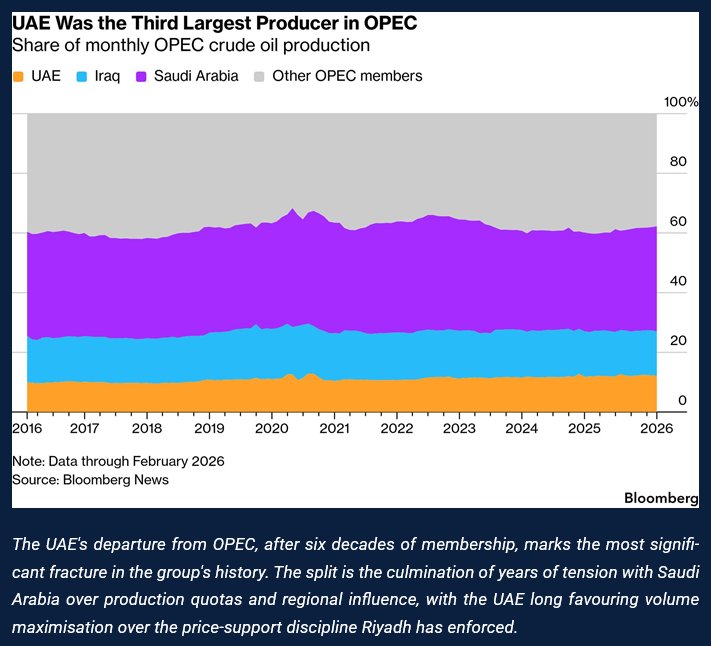

The Strait of Hormuz remains closed. Oil pulled back on Friday, with Brent crude settling at $108.17/bbl (-2%) and WTI at $101.94/bbl (-3%) on reports of an updated Iranian peace proposal delivered via Pakistani mediators. President Trump said he was not satisfied with the offer, keeping uncertainty firmly in place. Separately, the UAE announced it is leaving OPEC and OPEC+, citing a fundamental disagreement with Saudi Arabia over production strategy. The UAE favours volume maximisation ahead of the energy transition; Riyadh wants supply cuts to protect its fiscal position, a meaningful fracture within the world’s most influential oil alliance.

In Europe, the STOXX 50 ended broadly flat. The European Central Bank (ECB) held the deposit rate, its key rate, at 2% but acknowledged “intensified” economic risks and notably discussed a potential rate rise at length. The Bank of England held at 3.75%, flagging CPI at 3.3% and “highly uncertain” energy price prospects. The UK’s FTSE 100 Index was little changed, with most European markets, with the exception of the London Stock Exchange, were closed for International Workers’ Day on Friday.

In Japan, the Nikkei slipped 0.34% while the yen staged a sharp recovery from ¥160 to ¥156.7 against the dollar following suspected Ministry of Finance intervention. The Bank of Japan held at 0.75% with a hawkish tone.

In China, the Shanghai Composite gained 0.8%, supported by Moody’s revising China’s sovereign outlook to “stable”, while in contrast the Hang Seng declined 0.8%, reflecting softer offshore risk appetite ahead of the Labor Day holiday.

In the week ahead, the US–Iran diplomatic track remains the single biggest variable with global equities, bonds, currencies, and oil continue moving in lockstep with headlines. In the US, the payrolls report dominates the data calendar, while rate decisions are expected from Australia, Sweden, Norway, and Mexico.

Market Moves of the Week:

South African markets delivered mixed signals this week. The JSE All Share declined 1.2% for the week, dragged lower by resource counters, while the rand firmed 0.7% to close at R16.64 against the dollar as markets digested a batch of domestic data.

On inflation, the SARB is holding firm at its 3% target with Governor Kganyago explicitly ruling out any target adjustment despite the fresh oil shock working its way through the economy.

On the data front, producer inflation quickened to 2.3% year-on-year in March, up from 1.8%, with food, petroleum, beverages and tobacco the main contributors. Production costs are expected to rise further in the months ahead as the Middle East conflict keeps fuel prices elevated.

In response, National Treasury extended its fuel levy relief through to 2 June, with diesel receiving an additional 93 cents per litre of relief, reducing the diesel levy to zero. The general petrol levy remains at R1.10 per litre. The relief is designed to be fiscally neutral, with mechanisms to recoup the foregone revenue within the approved fiscal framework. Relief will then be halved and phased out through July.

On the political calendar, President Ramaphosa confirmed that municipal elections will be held on 4 November. The ANC enters the cycle in a structurally weaker position having lost its parliamentary majority in 2024 and governing through a broad coalition making local government outcomes a meaningful gauge of the political landscape heading into the next electoral cycle.

In a potentially significant structural development, the finance ministry has proposed a sweeping overhaul of South Africa’s capital flow rules including raising individual offshore allowances, regulating crypto assets, and allowing asset managers to run non-rand funds from a South African base for the first time. If implemented, the changes could meaningfully bolster South Africa’s standing as a financial hub for the continent.

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.