Global markets faced a turbulent week as the escalating conflict in the Middle East continued to overshadow economic fundamentals, driving oil prices above $100 a barrel for the first time in over three years. The blockade of the Strait of Hormuz, which is a critical artery through which approximately 20% of the world’s daily oil supply passes has sent energy prices sharply higher, rattling investor confidence across virtually every major asset class and region. Against this backdrop, slowing US economic growth and sticky inflation added to an already complex investment environment.

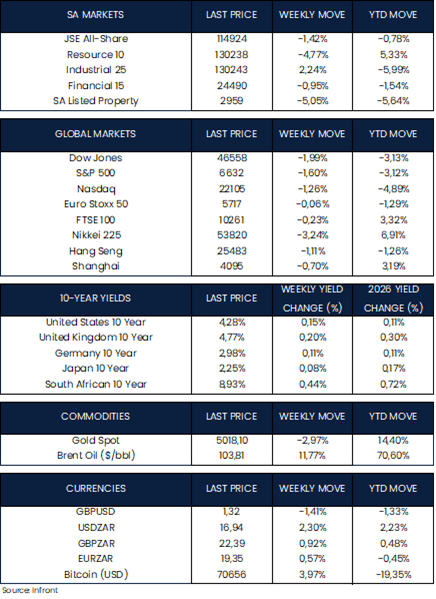

U.S. equity markets declined for a third consecutive week, with the benchmark S&P 500 ending the week 1.6% lower, recording its lowest level of 2026, while the Dow Jones Industrial Average lost approximately 2% and the Nasdaq Composite dropped 1.3%. Sentiment was further weighed down by concerns emerging in private credit markets, where several funds moved to cap withdrawals amid a wave of redemption requests.

On the economic front, the data was sobering. US GDP growth for the fourth quarter of 2025 was revised sharply lower to just 0.7% annualised, well below expectations and a meaningful step down from the 2.8% growth recorded in 2024. Core PCE inflation, which is the Federal Reserve’s preferred measure rose 3.1% year-on-year in January, running above the Fed’s 2% target. Critically, this data predates the Middle East escalation, meaning the full inflationary impact of energy prices is yet to be captured in official figures.

Consumer confidence also deteriorated, with the University of Michigan Sentiment Index falling to 55.5 in March, its lowest reading in three months, as higher petrol prices weighed directly on household budgets.

Oil prices were the defining market story of the week. Brent crude settled above $100 a barrel for the second consecutive session, reaching its highest level in more than three years, as attacks on oil tankers and Iran’s warnings of further escalation removed any prospect of a quick resolution. Governments moved swiftly to respond, with a coordinated release of strategic reserves estimated at approximately 400 million barrels globally, which is equivalent to roughly 3 million barrels per day, alongside US efforts to ease sanctions on Russian oil and provide insurance support for shipping in the region.

European equity markets demonstrated relative resilience, though caution prevailed throughout the week. The pan-European STOXX Europe 50 Index edged marginally lower, slipping just 0.06%, while the UK’s FTSE 100 declined 0.23%. Investor focus centred on the likely duration of the Middle East conflict, the trajectory of energy prices, and the potential knock-on effects for European economic growth.

With several major central bank decisions scheduled for the week ahead, including the European Central Bank and the Bank of England, markets are also beginning to weigh how policymakers will respond to an environment of slowing growth and renewed inflationary pressure from energy costs.

In Asia, Japanese equity markets came under meaningful pressure, with the Nikkei 225 Index declining 3.24% over the week. Japan, as a major energy importer, is particularly exposed to rising oil prices, and Prime Minister Sanae Takaichi announced the release of a portion of Japan’s strategic oil reserves and introduced subsidies to help contain the rise in domestic petrol prices. The Bank of Japan’s rate decision in the coming week will be closely watched for any signal on how policymakers intend to balance inflation concerns against fragile economic momentum.

Chinese equity markets also retreated, with the Shanghai Composite falling 0.70% and Hong Kong’s Hang Seng Index declining 1.11%. Despite the broader weakness, Chinese export data offered a bright spot with exports surging 21.8% in the January to February period year-on-year, well ahead of analyst expectations. Consumer inflation also accelerated to its fastest pace in over three years, boosted by Lunar New Year holiday spending on travel and tourism.

Gold, typically a beneficiary of geopolitical uncertainty, had another volatile week. Despite edging higher on Friday, bullion was on track for its second consecutive weekly decline, losing 3% for the week. Surging energy prices have paradoxically reduced expectations for near-term US interest rate cuts which is a headwind for gold, which tends to perform better in lower-rate environments.

In the week ahead the war in the Middle East and its impact on energy supply will continue to dictate global markets and will play a key part in a series of rate decisions from major monetary authorities. In the US, The Federal Reserve is widely expected to hold interest rates steady at 3.50%–3.75%. Investors will focus closely on the updated FOMC economic projections and Chair Jerome Powell’s press conference for guidance on how the Fed is navigating the tension between slowing growth and renewed inflation risks. Rate decisions from the ECB, Bank of England, Bank of Japan, Swiss National Bank, Reserve Bank of Australia, Bank of Canada, and several other major central banks will also feature prominently.

Market Moves of the Week:

South African markets came under renewed pressure this week, with the rand, equities, and bonds all weakening as the ripple effects of the Middle East conflict continued to weigh on emerging market sentiment. Rising oil prices pose a particular challenge for South Africa as a net energy importer, amplifying inflation concerns at a time when the domestic economy is showing tentative signs of improvement.

Amid the challenges, there was a welcome bright spot with South Africa recording its first current account surplus in more than two years in the fourth quarter of 2025, meaning the country earned more from exports than it spent on imports. The surplus came in at 0.6% of GDP, swinging from a deficit of 0.9% the prior quarter, driven by a sharp widening of the trade surplus from R169 billion to R282.2 billion. The primary catalyst was higher global prices for precious metals, with the increase in the gold price playing a central role.

The JSE All Share Index declined 1.42% over the week, with resource counters among the notable underperformers. The broader market has now fallen approximately 10% since the start of March which is a sharp reversal that, if sustained, would represent the market’s first monthly decline after an impressive 14 consecutive months of gains.

The rand extended its losing streak for a second consecutive week, closing at approximately R16.95 to the US dollar, over 2% lower than the prior week. The weakness reflects both the global flight from emerging market assets and South Africa’s specific vulnerability as a net oil importer, with further pressure likely should energy prices remain elevated.

Domestically, investors will focus on the release of January inflation and retail sales data from Statistics South Africa. Inflation figures will be particularly closely watched given the recent surge in global oil prices and rand weakness both of which feed directly into domestic price pressures. Any upside surprise in inflation could complicate the SARB’s monetary policy outlook and reduce the likelihood of near-term rate relief for consumers.

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.