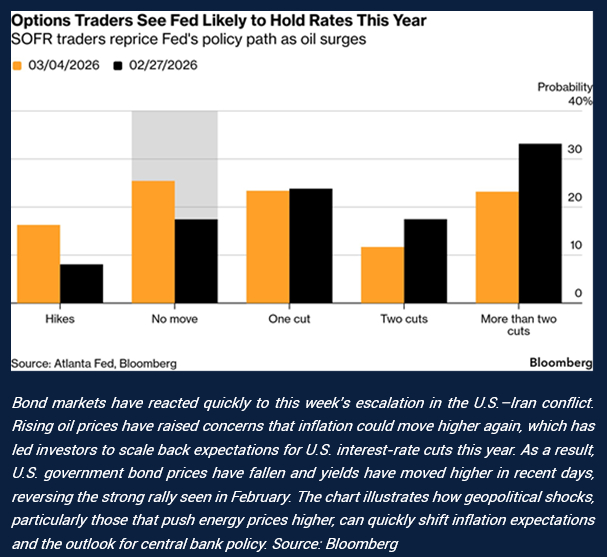

Global markets experienced a volatile week as a combination of geopolitical tensions and economic data created what many investors described as a “perfect storm” in markets. The escalation of the conflict in the Middle East following the United States’ military campaign against Iran pushed oil prices sharply higher, raising concerns about renewed inflation pressures at a time when global growth signals are becoming more mixed. Brent crude surged more than 30% during the week amid fears of potential supply disruptions, particularly as the Strait of Hormuz – through which roughly a fifth of global oil supply passes – faces potential disruption. Higher energy prices have historically been a challenge for both economies and financial markets, as they tend to lift inflation while simultaneously weighing on growth, a combination often referred to as stagflation.

The conflict has broadened into a regional confrontation, with Iran launching missile and drone attacks on several U.S. allies across the Gulf, while the United States and Israel have continued military strikes targeting Iran’s nuclear and military infrastructure. Attacks on vessels and energy infrastructure have already been reported, adding to concerns about the security of global energy supply routes. The human toll continues to rise, with casualties exceeding 1,000 people across the region. While diplomatic efforts have reportedly begun, the duration and ultimate scope of the conflict remain uncertain, leaving markets highly sensitive to further developments.

Against this backdrop, investors also digested a mixed set of economic data from the United States. Business activity indicators remained relatively resilient, with both manufacturing and services sectors continuing to expand. The ISM services index rose strongly to 56.1, its highest level since mid-2022, while manufacturing activity remained above the expansion threshold. Labour market data, however, sent a more cautious signal later in the week. Nonfarm payrolls unexpectedly declined by 92,000 in February, and the unemployment rate ticked up to 4.4%, raising questions about whether the labour market is cooling more quickly than previously anticipated. The weaker employment report complicates the Federal Reserve’s policy outlook, as policymakers must balance signs of slower growth against the risk that rising oil prices could push inflation higher again.

In Europe and the United Kingdom, investor sentiment also deteriorated as higher energy prices raised concerns about inflation and growth. European equities fell sharply over the week, with the STOXX Europe 600 index declining more than 5%. Inflation in the eurozone rose modestly to 1.9% in February, while unemployment fell to a record low of 6.1%, highlighting a mixed macroeconomic backdrop. In the UK, economic indicators suggested modest growth but ongoing fragility. Construction activity weakened and sterling fell to its lowest level in several months as markets assessed the potential economic impact of the conflict in the Middle East and rising energy costs.

Asian markets were similarly affected by the shift in global risk sentiment. Japanese equities declined sharply as investors assessed the potential inflationary impact of higher oil prices on an economy that remains heavily reliant on imported energy. Chinese markets were also weaker, with investors balancing geopolitical risks against domestic policy developments following the country’s annual National People’s Congress. Chinese policymakers set a GDP growth target of between 4.5% and 5% for 2026 and announced additional fiscal support measures aimed at boosting domestic demand and investment, particularly in technology and advanced manufacturing.

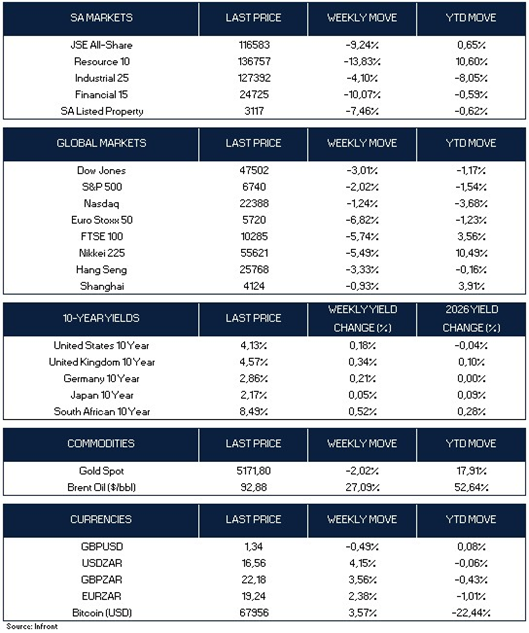

Overall, the week saw a broad risk-off move across financial markets. In the United States, the Dow Jones fell 3.01%, the S&P 500 declined 2.02%, and the Nasdaq eased 1.24%. European equities underperformed, with the Euro Stoxx 50 dropping 6.82% and the FTSE 100 falling 5.74%. In Asia, markets were also weaker, with Japan’s Nikkei 225 down 5.49%, Hong Kong’s Hang Seng declining 3.33%, and China’s Shanghai Composite slipping 0.93%. Bond yields moved higher across most developed markets, with the US 10-year yield rising to 4.13%, while UK and German 10-year yields increased to 4.57% and 2.86% respectively. In commodities, Brent crude oil surged 27.09% to $92.88 per barrel, reflecting supply concerns linked to Middle East tensions, while gold declined 2.02% but remains up 17.91% year-to-date.

Market Moves of the Week:

Recent economic data from South Africa presents a mixed but gradually improving picture. The manufacturing sector remains under pressure, with the ABSA Manufacturing PMI declining to 47.4 in February, signalling continued contraction. However, the S&P Global PMI held steady at 50.0, suggesting that activity across the broader private sector may be stabilising after a difficult period.

Business sentiment has shown some improvement. The Bureau for Economic Research (BER) business confidence index rose to 47 in the first quarter of 2026 from 44 previously – the strongest reading since 2015 outside of the post-COVID rebound. The improvement reflects a more stable political environment, supportive interest rate conditions and a relatively steady currency, although confidence remains below the neutral 50 level, indicating that businesses are still cautious about the economic outlook.

There have also been some encouraging developments on the investment and infrastructure front. A consortium of manganese producers is preparing a bid to build and operate a new export port at Ngqura in partnership with Transnet, which could significantly expand South Africa’s export capacity. At the same time, financiers are working on a R2 billion “water bond” aimed at funding projects to restore key water catchments and improve long-term water security. These initiatives highlight ongoing efforts to strengthen infrastructure and support the country’s longer-term economic resilience.

Local equities ended the week sharply lower, reflecting the broader global risk-off environment. The JSE All Share Index declined 9.24%, with losses broad-based across sectors. Resource stocks led the decline, falling 13.83%, while Financials dropped 10.07%, Listed Property declined 7.46%, and Industrials fell 4.10%. Despite the weekly weakness, performance on a year-to-date basis remains mixed, with Resources still up 10.60%, while Industrials (-8.05%), Financials (-0.59%), and Listed Property (-0.62%) remain slightly negative for the year. The rand weakened to around R16.56 against the U.S. dollar, while the South African 10-year government bond yield rose to 8.49%, reflecting the more cautious global risk backdrop.

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.