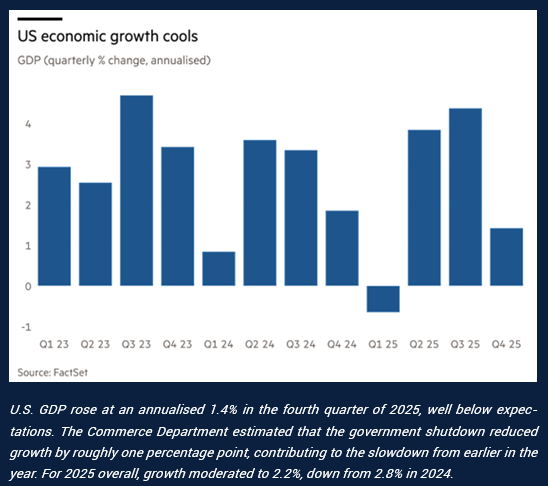

Data released by the Bureau of Economic Analysis (BEA) showed that U.S. growth slowed more than expected in the fourth quarter of 2025, with GDP expanding at an annualised 1.4%. The deceleration was largely driven by a sharp contraction in government spending amid the shutdown, which weighed on overall activity. Consumer spending remained comparatively resilient at 2.4%, though momentum softened relative to earlier in the year, while government spending declined 16.6%. For 2025 overall, economic growth moderated to 2.2% from 2.8% in 2024.

Separately, the BEA reported that headline PCE inflation rose 2.9% year-on-year in December, edging higher from the prior month and marking its highest level since March 2024. Core PCE — the Federal Reserve’s preferred gauge of underlying inflation, which excludes food and energy — increased 0.4% month-on-month and 3.0% year-on-year, accelerating from November’s 0.2% and 2.8%, respectively.

Minutes from the Federal Reserve’s January meeting, released on Wednesday, highlighted a clear split among policymakers over the next move in rates. While some members indicated that additional easing could be appropriate if inflation continues to cool, others pointed to “the possibility that upward adjustments” may be required should price pressures remain elevated. The minutes also noted that the “vast majority of participants” believe downside risks to employment have eased, though the risk of more entrenched inflation remains a concern.

In a 6–3 decision, the U.S. Supreme Court ruled that President Trump exceeded his authority in using the International Emergency Economic Powers Act (IEEPA) to impose tariffs on nearly all U.S. trading partners last year. President Trump responded critically to the decision and subsequently announced the implementation of a 10% global tariff, signalling continued intent to pursue an assertive trade stance despite the Court’s ruling.

UK CPI eased to 3.0% year on year in January, its lowest level in almost a year, partly due to lower fuel prices. Labour market data were also softer, with unemployment rising to 5.2% in the three months to December and wage growth slowing. The data have supported expectations that the Bank of England may cut interest rates at its March meeting, although inflation remains above the 2.0% target.

Seasonally adjusted industrial production in the eurozone declined 1.4% month on month in December, according to Eurostat, a sharper contraction than expected. In contrast, the preliminary February PMI surprised to the upside, with new orders expanding at their fastest pace in nearly four years

The International Monetary Fund expects China’s economy to grow 4.5% in 2026, slightly above its October forecast but below the 5% recorded in 2025. Following its Article IV consultation, the IMF noted that while growth has been resilient, structural challenges are intensifying and emphasised the need for a stronger shift toward consumption-led growth, supported by both macroeconomic measures and deeper reforms.

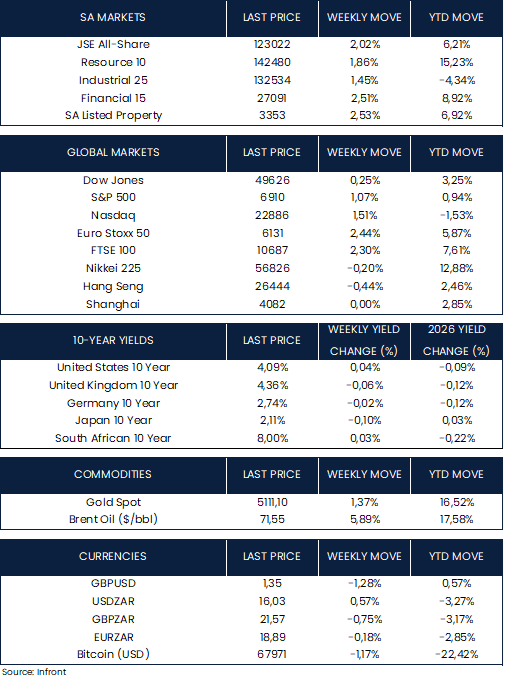

U.S. equity markets closed the holiday shortened week higher. The Nasdaq Composite led gains, advancing 1.51% and recording its first weekly increase since early January. The S&P 500 rose 1.07%, while the Dow Jones Industrial Average lagged the broader market, ending the week up 0.25%.

European equities delivered solid gains over the week, with the STOXX Europe 50 rising 2.44% in local currency terms. The FTSE 100 also advanced 2.30%, touching a fresh intraweek high.

In Asia, performance was more subdued. Japan’s Nikkei 225 edged 0.20% lower. Mainland Chinese markets were closed for the Lunar New Year from February 16 and will reopen on February 24. Hong Kong trading was suspended from February 17 to 19, following a half-day session on February 16, before resuming on Friday. The Hang Seng Index ended the week down 0.44%.

Market Moves of the Week:

Headline consumer price inflation in South Africa eased to 3.5% year on year in January 2026, down from 3.6% in December 2025, according to Statistics South Africa. The main contributors to the January reading were housing and utilities, food and non-alcoholic beverages, and insurance and financial services. Core inflation, which excludes food, non-alcoholic beverages, fuel and energy, increased to 3.4%, its highest in nearly a year.

Separately, Stats SA’s Quarterly Labour Force Survey reported that the official unemployment rate declined to 31.4% in the fourth quarter of 2025, from 31.9% in the third quarter, reflecting a modest improvement in labour market conditions. Overall, South Africa’s labour market shows improvements across multiple measures. However, unemployment levels remain exceptionally high, underscoring the persistence of the country’s structural jobs crisis.

The JSE All Share Index also ended the week in positive territory, gaining 2.02%, with broad based strength across all sectors. In contrast, the rand softened slightly, depreciating 0.57% against the U.S. dollar to close at R16.03 on Friday.

Chart of the Week:

As always, we appreciate your support and value your trust in LNKD Investment Managers.